Making a Distribution with the CheckBook IRA LLC

By Jordan Sheppherd

The subject of this post fits squarely within the bounds of a Frequently Asked Question. If you have an IRA, you’re going to eventually make distributions. If you’re of a certain age, you may be making distributions now. The question here is, how do you make a distribution with the CheckBook IRA structure?

It’s a common question, and one that can cause a bit of confusion because of the presence of the LLC. In this post, I’ll go over the specifics of how to make a distribution and talk about why it must be done a certain way.

Distributions from a Self-Directed IRA

If you have an IRA, you probably know what a distribution is, but it is helpful in this case to give a short review. A distribution occurs when a certain amount of money is paid out of an IRA to it’s owner. The IRA owner must then declare that distribution amount as income and pay taxes on it. Obviously, the funds that are paid out as a distribution lose their tax deferred protection. Think of it this way, once the funds leave the IRA and go into the IRA owner’s hands, two things happen: first, the funds lose the tax-deferred protection of the IRA and are treated as income to the IRA owner; second, the funds are no longer subject to IRA rules, which means the IRA owner can do whatever the heck he wants with the money.

Distributions & the IRA LLC

So how do you take a distribution if you have a CheckBook IRA? This can be confusing, especially if you’ve only recently been introduced to the concept of a Self-Directed IRA LLC. Because of the presence of the LLC, there’s an extra step when you take a distribution; and while it’s easy enough to grasp once you see it, it’s important you understand both the how and the why.

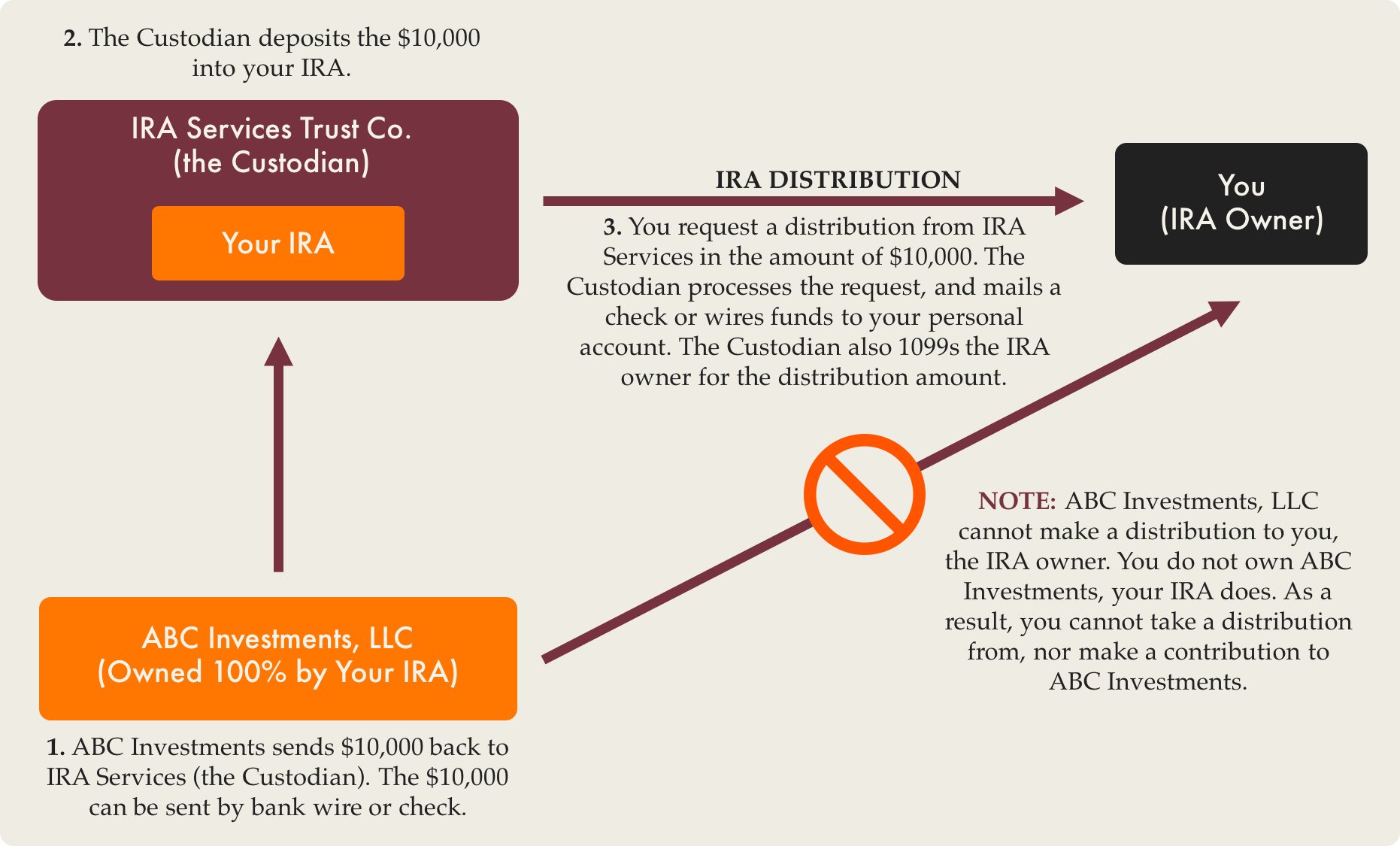

Let’s assume three things: 1. You already have an IRA LLC in place 2. You wish to take a $10,000 distribution 3. Your IRA doesn’t contain enough cash to cover the $10,000 distribution, as the majority of your retirement funds are in ABC Holdings, LLC.

Before we look at the chart, let’s pose a common question. Could you, as the Manager of ABC Investments, write yourself a check for $10,000 and call it a distribution? In other words, could the distribution be made from ABC Investments directly to you?

Let’s look at the following chart:

You can see from this chart that funds must flow up to the IRA first, and then to you. For a distribution to be considered a distribution, it must come out of the IRA itself. Think of the IRA as the gateway; if you want to make a distribution, the funds need to pass through the gateway.

ABC Investments would need to send funds back to it’s owner (your IRA). As the Manager of ABC Investments, you would send a $10,000 check or bank wire to IRA Services. IRA Services would deposit the funds in your IRA. You would then request a distribution from IRA Services. IRA Services then processes the distribution, cuts a check for $10,000 to you personally, and issues a 1099 to you for the distribution amount.

You declare that $10,000 as income for the year in which the distribution was made, and pay taxes on it the following April 15th.

A Common Misconception Corrected

Let’s return to the question I posed before we looked at the chart. I asked if ABC Investments could make a distribution directly to you, the IRA owner. I didn’t answer the question, but I hope you see that the answer is an emphatic “NO!”.

When people first begin researching the Self-Directed IRA LLC, it can be confusing for them to distinguish between their IRA and the LLC.

Let’s analyze the reasons why ABC Investments could not distribute funds to you, personally. By doing so, I think you will come away with a better understanding of the IRA LLC structure in general.

You, your IRA, and the LLC are all separate legal entities. In the eyes of the law, you are all separate persons. Don’t confuse yourself with your IRA; you’re separate. Don’t confuse your IRA with the LLC either.

Your IRA may own ABC Investments and it may own the entire company, but they’re still separate things. Your IRA is an IRA, and the LLC is a private company. I could write about 25 paragraphs on why this the case, but to save my hands from cramping up, to save you some eye strain, and in the spirit of Thomas Jefferson, who said “The most valuable of all talents is that of never using two words when one will do”, I’ve prepared a chart to show why this is the case.

Let’s take the chart from above and simply replace the name of ABC Investments. Instead of your IRA owning 100% of ABC Investments, LLC, let’s say your IRA owns $100,000 worth of Apple stock (sorry, I’m a Mac snob).

What would happen if you wanted a $10,000 distribution? Could Apple send you a check for $10k? Could you show up at the stockholder’s meeting and demand Tim Cook, the CEO, cut you a check for the distribution?

Obviously not.

You can see that the distribution would have to come from the IRA itself. In order to make the the $10,000 cash distribution, you would sell $10k worth of stock and bring the cash back to the IRA. The distribution could then be made.

It’s important to remember that you, your IRA, and the LLC, are all separate entities. The LLC may be owned by your IRA, but it’s no different than Apple, Inc. or any other company in the private sector. If you can grasp that, and keep it in mind as you go forward with the CheckBook IRA structure, you’ll be fine.

Invest intelligently. Enjoy the rewards.

Is it possible to distribute stock in the LLC rather than cash?

Astute question, Frank.

Yesterday I spoke with one of our clients in Arkansas who is planning to do just that. An IRA distribution may be made in any form, so long as the Custodian of your IRA will facilitate the distribution. Some of our clients choose to distribute property, gold or silver coins, or other tangible assets.

In this case, an appraisal of the LLCs worth would need to be done by a third party company to set the distribution amount. The Custodian would 1099 you for the dollar amount that the appraisal came out to, and a retitling process would need to be done to move ownership of the LLC into your name.

Note that some Custodians have rules regarding what assets they will and will not facilitate as distributions. We work with IRA Services Trust Company, which will facilitate pretty much anything you can think of, but if you plan on making the distribution through a different Custodian, make sure to check with them first to ensure they will allow it.

How do you feel about the idea of an IRA/LLC distributing real estate in-kind to the IRA owner – assuming the IRA custodian is “on board” and the property is appraised? As a tax attorney who has represented thousands of self-directed IRA investors, I have dealt with some IRA custodians who will accept this method and some that do not. The argument for allowing this is perhaps that there is very little difference between deeding the property from the LLC, back to the IRA, and then out to the IRA owner – versus – deeding the property directly from the LLC (but only if the IRA custodian treats the distribution from the LLC as a distribution from the IRA and reports the distribution to the IRS on Form 1099-R). On the other hand, deeding the property back to the IRA aligns more closely with the method that must be used in order to remove cash from the IRA/LLC. Thanks in advance for your comments!

My own feeling is that the property titling process should follow the same path as a cash distribution from the LLC, back to the IRA, then out to the IRA owner. That particular process may take more time, but it is more straightforward, cleaner, and the correct method in my opinion.

Have you run into any issues with clients who distribute property directly from the LLC?

One of the fundamental problems with the IRA/LLC structure is that some clients forget about the difference between the IRA and the LLC – which, of course, are legally distinct entities (despite the LLC being “disregarded” for federal tax purposes). For this reason, the best practice is for the IRA owner to have absolutely no interaction with the LLC. However, I have had several situations where Trust Company of America told IRA owners that taking a direct distribution of property from the LLC was acceptable – because TCA simply treated the distribution as though it happened out of the IRA. I agree with you – I do not like that method.

As a side note, I wonder whether states that impose excise taxes when real property is transferred (like my home state of Washington) would try and charge taxes on the transfer from the LLC to the IRA and then again when the property is transferred from the IRA to the IRA owner. Regardless, it is very rare that a lump sum distribution of a piece of real estate is a good idea from a tax or financial perspective – and hence, I generally discourage that type of “exit strategy”.

How is the property held within the IRA/LLC treated for tax purposes? In the case the property throws off a loss, can the individual (sole shareholder LLC) take the loss on his/her return without violating IRS rules on obtaining improper benefits?

Good question, J.A.

Since the owner of the IRA is a prohibited party, there could be no crossover at all between him and the LLC. Ultimately, losses are handled differently within the IRA LLC, but the IRA owner could not personally declare a loss that had occurred in the LLC, as the IRA owner, the IRA, and the LLC are all separate and distinct legal entities.

The assets and profits within the IRA, and in this case the LLC, are not taxed until they leave the IRA by way of a distribution. As a result, if the LLC were to own property and if that property were to throw off a loss for some reason, it wouldn’t be treated as a loss per se; the LLC (and by extension the IRA) would simply be worth less. It would be the same if the IRA purchased $10,000 worth of stock in a public company, and six months later, the stock lost 50% of it’s value, the IRA would not take a loss in the normal tax sense, it would simply decrease in total value.

Note that I am assuming the property within the IRA LLC has been bought with cash and has not been financed. If the property has been financed, it is subject to the UDFI rules, and any profits or losses would be handled differently.

Jordan,

Several years ago I opened a Checkbook IRA that has been very successful. In 2010 I converted it to a Roth IRA. At the time I had to supply IRA Services with a valuation. They sent me a 1099 for its conversion value and I paid the required taxes.. Since that time they have not requested any other valuation for my LLC which is owned by my Roth with them. Is this an oversight or because the Roth is no longer taxable a valuation is no longer required. Does the IRS still require a form sent to them by IRA Services for my Roth?

Hi Dale,

I’m glad to hear the CheckBook IRA we set up for you has worked well.

Generally IRA Services will ask for a yearly valuation for the LLC, even if you have a Roth. You should call them directly though, to see why they haven’t requested a valuation for the company.

Hello. I have a self-directed IRA, a single member LLC and checkbook account. The LLC owns a rental property and I’d like to own the property, personally. I understand I could take a lump sum distribution for the appraised value of the property. That’s a huge tax burden. Is there another way? Would it be more prudent to convert my self-directed IRA to a Roth IRA – pay the taxes then take control of my property. Or, is there an incremental way of taking more and more control of the property with the LLC having less control.

Neil

Hi Neil,

Whether you take the property as a distribution or whether you convert your account to a Roth and then distribute the property – you’ll end up paying the same amount in tax either way. There are ways in which the IRA can distribute a portion of the property with the idea that over X number of years, the property will be completely distributed and in your control. There are a number of ins and outs to that arrangement which generally includes bringing in a third-party property manager to manage the property until it is fully distributed, as the property will be jointly owned by you and the LLC in the interim.

I don’t know who your Custodian is, and what their internal rules are regarding this type of distribution arrangement. If you’d like to chat at more length, you can call our office at 1-800-482-2760.

Rental property held by llc. Could you setup a Roth Ira and do a distribution in kind to the Roth 10% per year after 10 years the Roth would own 100% of the Rental Property and be tax free income for you or your heirs

Hi Robert,

Do you mean an LLC that is owned by you that has this property? If so, the answer is no. You can only contribute cash to a Roth IRA; you can’t contribute property to a Roth IRA. You can do it with a Roth 401(k) though. The rules are different with 401(k)s, and there is a way to contribute property to the Roth component of a Solo 401(k), and the contribution limits are much much higher, so you wouldn’t have to spread it out over 10 years, necessarily.

Jordan:

Thank you so much for responding to my question. I will call your office this week.

Neil

FIrst of all, thanks for the great blog. Very informative and thorough.

I have a series of questions each building on the next. (This is a fictional example.)

Let’s assume I have a self-directed IRA, a single member LLC and checkbook account.

I fund the IRA from a roll over with 200K. I ask the custodian to buy the entire LLC for 200K.

1. Can I issue from the LLC to the IRA 1000 little shares of this LLC instead of just one big share.(in both cases equalling 100% of the LLC)?

2. Can I buy, with cash from the LLC, a house (say for 100K) and title it in the name of the LLC (only)?

3. Years later when the required minimum distribution (RMD) kicks in, can I have the custodian distribute a portion of the shares of the LLC to me? Of course at this time both myself and my IRA would co-own the LLC.

Dave,

Good questions. I’ll take them one at a time.

1. The LLC can certainly issue membership units to the member in any denomination. It doesn’t matter if you issue one unit worth $200k, or 1,000 units worth $200 each.

2. Yes. The LLC could purchase a house for $100k, and the house would need to be titled in the name of the LLC, and only the name of the LLC – unless you’re partnering with someone or doing a joint venture.

3. Technically, the Custodian could distribute a portion of the membership units to you. I’ll be quick to note that I would not recommend this. Its a tricky subject, and one that would require much more space than just a comment on a blog, but it would probably be considered a prohibited transaction to distribute the units to you, unless the Operating Agreement addressed this eventuality. Even assuming it could be done without triggering a prohibited transaction on the distribution itself, you end up in a position where you and your IRA co-own the same LLC. This creates a nightmare because any transactions in the future would have to closely scrutinized to ensure no prohibited transaction occurs, and it almost certainly would.

A few of our clients have arranged for the distribution of the LLC ownership in one fell swoop. That is a different story, because the entire ownership is coming out to the IRA owner, and no entangling relationship exists between the IRA and IRA owner after the fact.

Hi. Thank you for your blog. The information and advice you give is spot on. I will probably ask my custodian if I can convert my checkbook IRA-LLC to a roth. The only problem I see is it’s holding silver eagles in a depository. I am worried how they will be appraised. Again, thank you.

For gold and silver coins, Custodians will use spot prices to figure the value. With Eagles, they have to figure in the premium, so its a good idea to check with your Custodian to see how they peg that value. Some Custodians will look to a big firm like APMEX or KitCo for Eagles prices, while others have a different way of doing it.

With silver dipping like it has, it might be a good time to consider converting. Just make sure you talk with a knowledgable CPA who can give you a good idea of what kind of tax hit you would take from the conversion.

Finally, even if you have existing metals in an IRA, there is a way to move those metals to the LLC without having to sell the coins.

Hi Jordan, Thanks for establishing this informative blog. With the discussions of converting a checkbook IRA to a Roth IRA, is there a way to do it incrementally? In other words, over the next four years, I’d want to take partial distribution from the IRA to fund a newly established Roth IRA, but still maintain the LLC, as it would still keep funds for the regular IRA. How would I go about obtaining checkbook control for the Roth IRA? Could the current LLC foundation documents be amended to allow this, or would I need a new LLC set-up? Thanks.

Hi Sam,

Its certainly possible to convert incrementally to a Roth IRA. A new LLC could be formed for the Roth. Its possible that the Roth could come into the existing LLC, although that can get a little tricky. Why don’t you give me a call when you get a chance, and we can go over your options. You can reach me at 1-800-482-2760.

How can I purchase gold or silver with my checkbook IRA LLC and not have it held by a third party? In other words, I want to have the commodity in my possession in case of an economic collapse.

Hi Clark,

Gold, Silver, and Platinum American Eagles can be bought with an IRA-owned LLC, and stored by the Manager of the LLC, or at some other location of the Manager’s choosing.

Those coins would be owned by the LLC, so you can’t use them personally, or derive any benefit from them, but you can store them at home. Should you choose to sell those coins at some point in the future, it would be the LLC that is selling the coins, and whatever dealer or person you’re selling the coins to, would send funds for the purchase to the LLC’s bank account. At that point, you are able to reinvest those funds into something else; always in the name of the LLC of course.

Hello Jordan,

What if I want to take a distribution and all the IRA funds are gold and silver eagles that I, as the manager, are storing? Do the coins have to be converted back to cash?

Hi Lilly,

Thankfully, you don’t have to sell the coins and convert to cash; the coins can be distributed in-kind, so long as the LLC has been set up properly. The value of the coins that are being distributed will be the value of the distribution, and the Custodian will send you a 1099 at the end of the year for that amount.

Thanks for the question.

I am considering moving funds in an existing IRA to a checkbook IRA investing in home-held silver.

My question is a little bit of a twist on Clark’s question.

I am a few years away from being able to take distribution without penalty. So if in those years, silver price rise to the point I would want to sell, can I sell and keep cash in the IRA? Or would that be considered a distribution subject to taxes?

Mike,

Once you reach 59 1/2, you’re eligible to take distributions without an early withdrawal penalty, but you are not required to take distributions. Once you get up to 70 1/2, you’ll have to start taking distributions, but even then its a minimum amount each year.

At any time you could sell the coins and bring your account either entirely or partially to cash – that is not a taxable event; its the same as if your IRA owned stock in Apple, Inc. and then sold the stock – the cash just comes right back to the IRA and sits there until you decide to make another investment. Its the same here with the IRA LLC. As a side note, you would also have the option of distributing the coins themselves, as opposed to cash.

I don’t see the following issues addressed anywhere on your otherwise excellent site. What happens to the IRA-LLC upon death of the IRA owner? Can the beneficiary spouse ‘roll-over’ the entire LLC to her own SDIRA and have it appoint her the manager?

If the IRA beneficiary designation lists percentages to others (e.g. children), besides the spouse, and the LLC was created with shares of stock (evenly divisible by the percentages assigned to the beneficiaries – e.g. 60% to the spouse, 10% to each of four children), could each beneficiary ‘roll-over’ their share of the LLC into each’s own SDIRA, but with the LLC still being managed by the spouse (or just one of the beneficiaries)? Would this require changing the LLC into a partnership, and if so, how difficult would this be?

Eventually this gets real messy: The surviving spouse takes distributions of her share as required by the IRS. If she lives long enough to deplete her share before passing, does she cease to be a partner? If the other owners continue to take distribution to support the mother, presumably they pay the early-withdrawal penalty on those distribution. But if value remains in the spouse’s share upon her death, does that remaining portion of the LLC then pass to the other beneficial owners’ portions of the LLC in their SDIRAs?

Thanks!

Oldman John

Hi John,

Good questions. I won’t be verbose with my reply, other than to say these are pretty common estate planning issues, and there are ways to handle these issues, but it all depends on a guy’s situation; what he has to work with, and what he wants to accomplish.

One of the easiest ways to handle it, is to form a trust as the 100% sole beneficiary of the IRA. The wife, and kids can be beneficiaries of the trust, as well as trustee(s). That handles the messy situation of having multiple owners of the LLC, once the original IRA owner dies, because the trust inherits the IRA, and everything the IRA owns. The LLC would still be considered a single-member disregarded entity, and the management of the LLC could be handled by the trust’s trustees, or some other party.

Jordan:

Is it possible to take bonus money a company gives to you and put this money in your Checkbook IRA account?

How much can you invest in your Checkbook IRA?

I am over 59 1/2 years old.

Hey Jack,

To make a contribution to an IRA, you have to have earned income. A bonus from your company is earned income, so you could put some of that into the IRA as a contribution. Since you’re over 50 years old, you could contribute up to $6,500.

Can the earned income be from a retirement pension that includes a social security supplement in the monthly payment? I’d like to continue to make contributions to my checkbook IRA once it’s established. If I’m under 59 1/2 what is the annual amount I can contribute? And would this have to be contributed through the custodian?

Hi Jackie,

In order to qualify to contribute to an IRA, you must have earned income. Pension payments and social security doesn’t count as earned income, so if that’s the only income you have, you wouldn’t qualify to contribute to an IRA.

The contribution limits to an IRA depend on whether you’re under 50 years old or over 50 years old. If you’re under 50, you can contribute $5,500. If you’re over 50, you can contribute $6,500.

The contribution would have to be made directly to the IRA, so you’d have to fill out the Custodian’s contribution form, and send the funds to them so they can deposit the contribution into your IRA.

Hope that helps 🙂

Aloha Jordan,

I really wish I had “found” you before I signed up with another registered agent of our IRA accounts. I have given up on getting answers from that agent – multiple emails, phone messages, and no responses leave me searching for answers on my own, and I really appreciate this blog and your kindness in answering all inquiries.

I was told, years ago, that I could only fund a checkbook IRA LLC once. Is that still true? Over the years, the LLC invested as a hard money lender and made money when the funds were paid back with interest, so the funds in the checkbook LLC grew a little each time. Now, I want to increase the LLC funds with more IRA money (sitting in IRA Services Trust) that was contributed each year. Can I?

Also, another one of my checkbook IRA LLCs has some money, but not enough to invest in real estate. I want to deposit that money into my Ameritrade Roth IRA account so I can trade stocks/options with it, hopefully increase the value of it (big hopes that it goes way higher), then put it back into the checkbook IRA LLC. Can I do that by depositing it from the checkbook IRA LLC into the Ameritrade account (that is in my personal name) or do I have to transfer it back to IRA Services Trust and have them deposit it to Ameritrade?

Mahalo (thank you) for your expertise and helping us with such solid information.

To your first question: Given that I was just quoted a specific price today — by IRA Services Trust — for subsequent transfers into the checkbook IRA (which in turn is conveyed to the IRA LLC’s bank account), by definition it can’t be true that (at least in the general case) you can only fund a checkbook IRA LLC once. Hopefully that’s good news…

To your second question: There are really two issues at play; first, does the money have to be conveyed, either via trustee-to-trustee transfer (“direct rollover”) or via 60-day rollover, through IRA Services Trust (yes, it does); second, what is the best way to handle the situation where one account is a Traditional IRA, while the other account is a Roth IRA (which incurs the overhead of “conversion” in one direction, and “recharacterization” in the other)?

Incidentally I did not ask IRA Services if they charge money for trustee-to-trustee transfers. I will add that to the to-do list, for all of the trustees I am evaluating. (The Fidelitys of the world never mention those nickel-and-dime fees, and I assume it’s “free” for them, but for trustees who hold our money, they may have to charge a small fee to cover their costs.)

If it’s to your advantage to hang onto the money personally for up to 60 days between custodians, then so be it, but just be aware of the new rule (since 2015) that allows you to do only one of these — across all of your IRA accounts — per calendar year. (On the other hand, there are no limits to the # of trustee-to-trustee transfers.)

To actually do the Roth conversion on the way in, Ameritrade will probably insist on creating a ‘Rollover IRA’ for you (at no charge) and then perform the Roth conversion of the funds into your Roth IRA within the Ameritrade umbrella, after which you can close out the Rollover IRA. That should just be a formality; the real issue is, the conversion itself is a taxable event, and you will owe any tax due on the overall ratio of pre-tax to post-tax money across *all* of your Traditional IRAs (not just the one you are transferring the money out of).

One point to be aware of is that, the Roth 5-year rule on conversions will apply so that, if you changed your mind and decided to hang onto your Roth funds for eventual distribution, even if you reach >59 1/2, you will not be completely liberated from tax consequences for up to 5 years (though to really understand how it works, look for material online and read the fine print!).

However, that shouldn’t affect you if you decide to move the funds back to your Traditional IRA within the time limit for recharacterization, which is roughly October 15th of the following tax year. Roughly speaking, that unwinds the conversion as if it never happened. (You’ll have to file an amended return, among other things.) If you miss this date, then your money will be stuck within the Roth framework — according to the IRS, “Roth IRAs can only be rolled over to another Roth IRA.” If you want to start self-directing this investment money, unless I’m mistaken, it will require you to set up a checkbook Roth IRA LLC.

Pardon me — I meant to say, “for trustees who *don’t* hold our money…”

Mahalo for your reponses, Not a Guru.

A phone call with IRA Services Trust cleared up the question of being able to fund a Checkbook IRA LLC more than once. The reason that I use them is that they have the lowest fees, and they are nice people.

A phone call with Jordan Shepard (wonderful people!) helped with the Ameritrade trading accounts, as well as chatting with Ameritrade people. Conversions between regular IRA to Roth IRA accounts are easily done, but the name on the accounts need to be the same. I fill out a deposit form and mail it in, since it needs a “wet” signature. I find that easier to do than having a 60 day conversion dilemma because I might forget to do the right things at the right time. Ameritrade then issues me a 1099 for the conversion.

To have my checkbook IRA LLC account have an Ameritrade account, I needed to open a new account in the name of the checkbook IRA LLC, not my personal name. Then, IRA Services Trust sent Ameritrade a check (no wire transfers in this case) using funds that were “sitting” in the LLC’s account. Prior to that, I wrote out a check from my checkbook IRA LLC to IRA Services Trust so the money was available for them to send out to Ameritrade.

It sounds like a complex series of transactions, but Jordan’s explanation about each component is separate from each other made it crystal clear. When I sell the stock holdings in the Ameritrade checkbook LLC account, it can either sit there as cash, or they will send out a check (or transfer) to IRA Services Trust for the LLC account. From there, IRA Services Trust will send out a check to me from the LLC account, which I then I deposit in my IRA checkbook LLC bank account.

This is a very informative blog, thank you.

In the first example of a $10,000 distribution created by the IRA owned LLC sending $10,000 to the custodian, then the custodian distributing it to the IRA Owner how does the LLC characterize this transfer of money back to the IRA. Is it a dividend? Is there tax reporting that the LLC needs to complete as part of sending funds back to the IRA? My initial thought is no tax reporting since the LLC currently does not report rather it provides annual value back to the custodian.

Example being used:

Let’s assume three things: 1. You already have an IRA LLC in place 2. You wish to take a $10,000 distribution 3. Your IRA doesn’t contain enough cash to cover the $10,000 distribution, as the majority of your retirement funds are in ABC Holdings, LLC.

ABC Investments would need to send funds back to it’s owner (your IRA). As the Manager of ABC Investments, you would send a $10,000 check or bank wire to IRA Services.

Hi John,

Thanks for the compliment; I’m glad you find our site useful.

In the example you use, the LLC would simply be making a distribution of the member’s accumulated cash. I suppose you could call it a member distribution. That is, the LLC is distributing funds to its member (owner). Either way, it isn’t reportable because as you pointed out, the LLC has no Federal filing requirements. It would reduce the value of the LLC of course by the amount sent, so the next year, the valuation sent by the LLC’s Manager back to the IRA Custodian would reflect that.