IRS Filing Requirements for a Multi-Member CheckBook IRA LLC

In an earlier post entitled IRS Filing Requirements for a CheckBook IRA LLC, I explained why a single-member IRA LLC or an LLC with one IRA as the owner was not required to file a Federal Tax return (assuming the LLC did not incur any Unrelated Business Taxable Income). But what happens if the LLC has multiple members or owners?

This article will be considerably shorter than the last one, for the simple reason that I laid a lot of groundwork out in my earlier post, and there’s no need to rehash it here. I suggest you glance through the earlier post before you read this one. Please note that I am assuming that the multi-member LLC did not incur any Unrelated Business Taxable Income.

I’ll give you the bottom line first, and then we’ll work toward the how and why of it.

Bottom Line

A multi-member IRA LLC must file a Form 1065 Partnership return, and also complete a Schedule K-1 for each owner of the LLC.

A partnership is a flow-through entity.

Partnerships

So that we don’t confuse our terms, it is important to remember that there are many types of “partnerships”, from General Partnerships, to Limited Partnerships, to Limited Liability Limited Partnerships (a bit of an awkward name, that one), and others. Each of these partnerships are statutorily defined entities that are formed for specific purposes (read: doctors, lawyers, dentists, construction companies, etc…). In this case, however, we’re not talking about one of those entities, we’re dealing with a Limited Liability Company (LLC) with two or more owners. The reason why I’m using the term “partnership” to refer to this structure, is that the IRS will treat the LLC with two or more owners, as a partnership for tax purposes.

To put it more succinctly, while all of those partnerships may be different from each other, and from an LLC with multiple owners, all of them are classified as partnerships for tax purposes, and have the same filing requirements. To put it even more succinctly, in the eyes of the IRS, all of them are the same when it comes to filing requirements.

A partnership is a flow-through entity. This means that as the partnership earns income, it passes the tax liability of that income back to it’s owners. The partnership itself never pays taxes. Every partnership must file an informational tax return, and prepare income statements for all the owners of the company. The return itself is IRS Form 1065; the income statement to the owners is Schedule K-1.

Partnership Example

Let’s look at an example to see how this works in a normal situation:

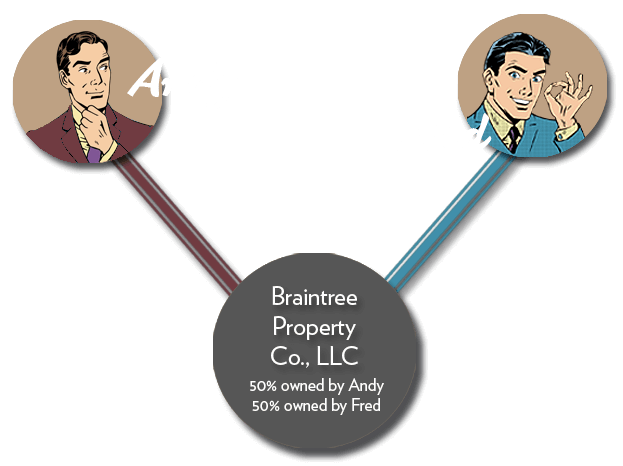

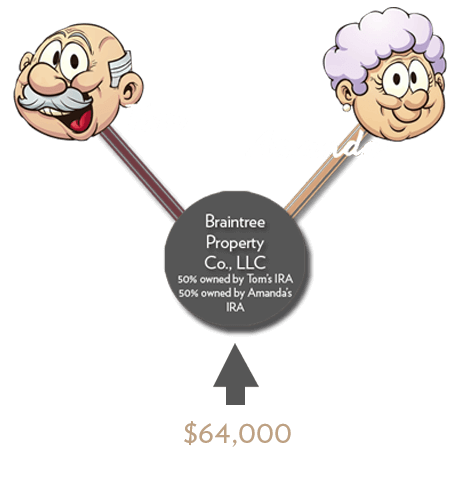

Andy and Fred decide they would like to invest in real estate. They don’t want to do it individually, but would like to partner up and take advantage of combining their funds to buy and hold rental property. They formed an LLC named Braintree Property Co., of which each of them own 50%. Since the company has two owners, the IRS will treat this LLC as a partnership for tax filing purposes.

Now let’s fast forward to the end of the year:

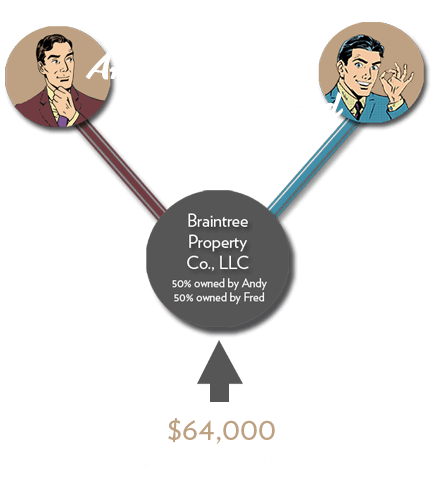

We see that in the course of the year, Braintree Property Co., LLC has bought some property, and earned a total of $64,000.

Here’s how the filings would go:

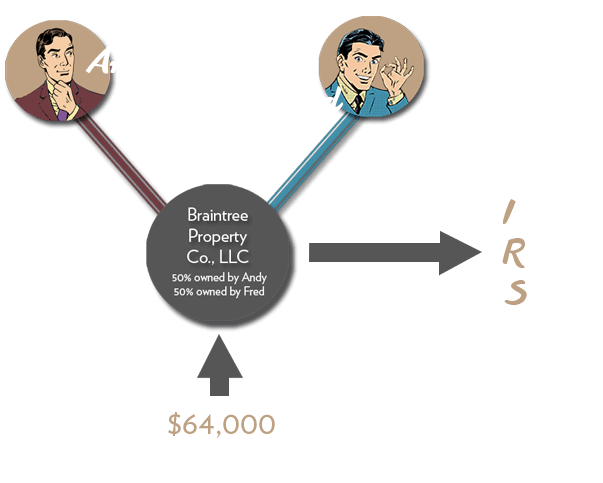

- Braintree Property Co., LLC would file a Form 1065 with the IRS to report the earnings of the company itself. No tax would be due here, remember; this is just an informational filing.

- Next, Braintree Property Co., LLC would complete two Schedule K-1 forms – one for Andy and one for Fred. The K-1 forms would show the respective share of the income for each owner, which in this case would be $32,000 to each. Andy and Fred would both have to declare, and pay taxes on, the $32,000.

- In real life, Braintree Property Co. would be able to write a number of things off which would reduce the amount of income, but this is just for illustration purposes.

* While the partnership would file the 1065 Partnership Return, the partnership itself would owe no tax. The tax liability is passed to the owners of the LLC by way of the Schedule K-1.

* The Schedule K-1 acts like a 1099; it shows the amount of income Andy and Fred have made as a result of their ownership in the LLC. In this case, Andy and Fred would each receive a Schedule K-1 for $32,000.

IRA LLC Partnership Filing Example

With that in mind, let’s simply lay the IRA LLC structure over the top of our earlier example.

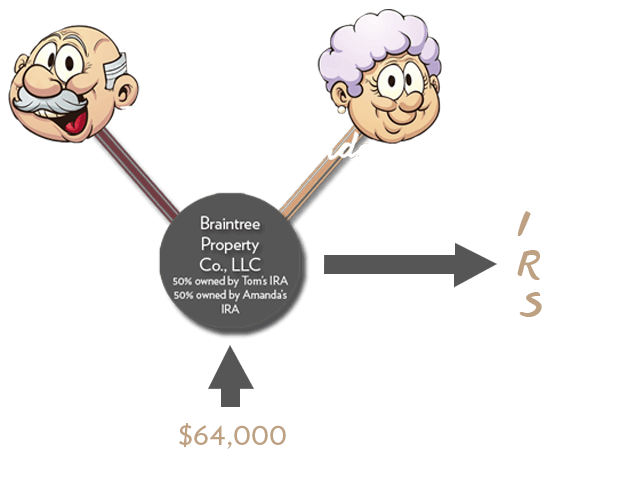

Here, we have a company named Grey Hair Holdings, LLC. This company is owned by two IRA accounts; one belongs to Tom, and the other belongs to his friend Amanda. Let’s not change anything else from our example above.

This LLC is going to buy rental property, and throughout the course of the year it earns $64,000.

You can see it’s the same as before. Grey Hair Holdings, LLC files a Form 1065 with the IRS, and prepares Schedule K-1s for Tom’s IRA, and for Amanda’s IRA. Like any other informational return, two copies of the K-1 must be sent out: one to the IRS, and one to the owner of the entity. So in this case, a copy of each K-1 would need to be sent to the Custodian of Tom’s and Amanda’s IRAs.

Because an IRA enjoys tax-deferred status (or tax-free in the case of a Roth), the income earned by Grey Hair Holdings, LLC would not be taxable to Tom’s and Amanda’s IRAs. The IRAs’ tax deferred status would cancel out any income that would otherwise be taxable. Remember, we’re assuming Grey Hair Holdings has not incurred Unrelated Business Income Tax.

Other Examples

If you are in a situation where there are more than two owners of an LLC, or there are mixed owners in the sense that some of the owners are IRAs and others are persons or entities – the same concept applies. The bottom line is that the partnership itself files a Form 1065 return, and then prepares Schedule K-1s for each and every owner of the company, irregardless of the type of owner (IRA, person, other entity).

You should have a competent CPA handle the filing, unless you’re intimately familiar with all of the ins and outs of a partnership return. This article is intended only to provide a conceptual overview.

As always, should you have questions, please feel free to comment below.

Invest intelligently. Enjoy the rewards.

For the multiple-member LLC IRA,

in addition to filing a K-1 for each member with the 1065 to the IRS,

is the K-1 sent to the respective IRA owner/member or the Custodian of the IRA?

The K-1 is generally sent to the Custodian of the IRA, although you might check with your Custodian to confirm how they handle it.

Hi

thank you for the post

but who can sign the return?

Tom and Amanda are not partneres in the LLC partenship

Hi Alon,

You should check with your Custodian to see how they handle this. Some Custodians will sign on behalf of the TMP member, since there is no “member-manager” of the LLC. Some Custodians will actually allow the IRA owner to sign the return, as the IRA owner becomes a fiduciary to the IRA when he/she opens a self-directed IRA; although that’s not always the case, so its a good idea to check the plan documents/agreements of the Custodian. I think its a bit of a stretch to say the IRA owner can sign the return, although there is an argument to be made there.

Keep in mind that I wrote this article to give people a general idea of how the filings would go; its not intended as an exhaustive study of the subject, and we don’t offer tax advice.

thanks

it was very helpful your post

i think the signture issue are still

in the grey area

thanks

I agree its in the grey area to say the IRA owner can sign the return, but the Custodian is the trustee to the member(s), so its fine for them to sign.

Thanks for your question.

Jordan,

This is really an excellent article! I’m going through the throes of preparing tax forms now for my multi-member LLC and have a couple of questions about them.

1) A general question. You gave an example of two friends, Tom and Amanda, who joined IRAs to form an LLC. I thought, though, that only IRAs of spouses can join to form a self-directed IRA LLC. Is this the case?

2) Another general question. You presented a case of “mixed ownership” of an LLC in which some of the owners are IRAs and others are persons or entities. I didn’t think this was allowed since there are numerous restrictions for IRA owners by which non-IRA entities are not bound. Can you clarify this as well?

3) I formed my LLC in 2011 that has two IRA owners. I did not have unrelated, debt-financed income in 2011 but didn’t realize that I had to file a partnership return and K-1s anyway for this year. What are the consequences for not having filed in 2011? In 2012, I did have unrelated debt-financed income that necessitated 990-Ts for the owners, which also “pinged” me to prepare a partnership return and K-1s for the IRA owners. I was thinking of checking the box for the partnership of “initial return” to avoid hassles due to not having filed in a return in 2011. What do you think?

4) Your article didn’t address the requirements to file partnership returns, K-1s and 990-Ts with the states. It might be a good subject for another article since there are apportionment and allocation issues of owning assets in two or more states.

Hi Rich,

Thanks for your comment. I’ll answer your questions in order:

1. There are no restrictions on multiple IRAs coming together into one entity. For example, if me and my best friend were to find an investment, our IRAs could purchase the same LLC, and become partners in that LLC. When someone wants to do a multiple-member IRA LLC, they generally want to set it up with their spouse, but there’s no restriction that it has to be a spouse. In fact, it is much better to have a multiple-member IRA LLC with people who are not related to each other, as you don’t run into some of the complications of a spouse multi-member IRA LLC. Since the husband and wife are prohibited parties, there is a level of complexity in the setup and maintenance of the LLC, that would not be present if say, two friends were to set up an IRA LLC together.

2. There aren’t restrictions either on mixing owners of the IRA LLC, except for prohibited parties. As a result, the ownership of the LLC can be a mixture of IRAs, people, corporations, other LLC, etc… So long as the prohibited transactions rules are followed, which is to say that so long as there are no prohibited parties present as owners (or if so, the ownership is small enough) there is no problem with many persons/entities owning the LLC. Obviously this is a pretty generalized response to your particular question. When multiple people/entities come together to own an LLC, and IRA among them, it is always important to review everything to ensure no prohibited transaction will take place.

3. Have you secured an EIN for the LLC? If so, look at the start date of the LLC. When you apply for an EIN, you list the starting date of the LLC. If the starting date was last year, you’ll probably need to send in a 1065 for last year anyway. You should check with your CPA.

4. We generally don’t get into State filings, because with so many jurisdictions, its better to go to a CPA who is familiar with that particular State’s requirements.

Hi Jordan:

Thanks for all of the great info, it is most helpful!

I wonder if you could provide any insight about an article (link below) in which the author surmises that if you are the IRA owner and perform the bookkeeping services of your IRA owned LLC that you are making an excess contribution and engaging in a prohibited transaction.

Specifically, this section is concerning: “Although there are some exemptions for services provided to a retirement investment plan, they do not extend to services provided to entities owned by the plan.”

Should I be concerned that the IRS will take issue with me doing the books of my multi-member LLC?

Thanks in advance,

Chris

(https://newdirectionira.com/irs-on-red-alert-checkbook-ira-llc-may-cost-big-retirement-money/) that

Hi Chris,

Thanks for the question.

The article you linked to is interesting in that it doesn’t give a link or any other information about the internal memo that the Services issued to it’s field agents. Not to say that no such memo was issued, but it is important to see the memo itself to see what the actual issues are.

For example, were the contents substantially similar to the listed transactions for Roth IRAs in IRS Notice 2004-8? If so, then this is old news. The IRS, over the last number of years, has fleshed out this issue, especially regarding Roth IRAs. Here is a good example of what they’re talking about.

The question becomes, what does the Service consider “services”? Its pretty simple in a single-member IRA LLC, as there are no Federal filing requirements for that kind of structure, so any accounting or tax-related services would be at a minimum. A multi-member IRA LLC must file the 1065 partnership return and prepare K-1s, so the time involved is greater. If a tax return is required, its always a good idea to have a professional do it for you.

Doing the books, though is a different matter. In the absence of a particular ruling, on this particular subject, we should always look to the spirit of the law and try to follow that. The spirit here is that the DOL and IRS do not want an IRA owner to do a bunch of work for his/her IRA or IRA LLC, so that value is added to the account that would have otherwise been used on expenses to pay for the services rendered by the IRA owner.

Let’s use an example: Bill and Martha (spouses) have a multi-member IRA LLC. The LLC owns 15 properties, 7 of which are multi-unit properties. Bill is the Manager of the LLC, does not employ a property manager, and handles all the day to day transactions when it comes to repairs being made on the houses. Is Bill doing too much? I think its pretty clear that he is. The problem here begins with size; the LLC owns so many properties, that in the absence of a property manager, its difficult to say that the time required for Bill to handle all the properties is within the spirit of the law. Next, instead of employing a handyman or contractor to handle the repairs on the properties, Bill is running around trying to do them himself. Again, its pretty clear he’s stepped over the line. Finally, in this scenario you can see that keeping the books for this kind of arrangement, where everything is handled by Bill, would be prohibitively time consuming. When you add up the money that is saved by Bill not hiring a property manager, not hiring a handyman/contractor to handle the repairs, and not hiring a bookkeeper for all of these properties and transactions, this is the kind of money that starts to add up. You can see that in this case the Service would no doubt consider Bill’s time and effort to be a shift in value from him to the LLC.

With that in mind, the question you should ask yourself is “Are the holdings of my IRA LLC substantial enough that I am devoting too much time and effort in doing the books?” For most people the answer will be no, unless they have a very large account, and have a large number of holdings. The average IRA LLC owner is not in a position where handling the affairs of the IRA LLC is so demanding that he would be required to hire out doing the books, or that the Service would view his time spent doing the books as an excess contribution or prohibited transaction.

Also, remember that the role you play as the manager of the LLC is exactly that, as the Manager of the LLC. So when they talk about exemptions that do not extend to the services provided to entities owned by the plan, that is irrelevant, because you are not keeping the books as the IRA owner, you are keeping the books as the Manager of the LLC. Those are two entirely different roles.

That is very helpful – I appreciate your response. Your example is very helpful.

As a follow up question, if a portfolio of assets were to grow over time such that the IRS began paying more attention, is the statute of limitation still the three years (six if income was understated by more than 25%)? Also, is there a statute of limitation as to the IRA becoming taxable and penalized?

Thanks again,

Chris

I’ll be honest, Chris – I don’t actually know. Our clients have never had a problem with excess contributions or prohibited transactions, so its never been something we’ve had to deal with. Having said that, I should probably know the answer, so I’ll do a little research.

Have a good weekend 🙂

Are husband and wife IRA owners of a multi member LLC in a community property state still considered a disregarded entity for federal tax purposes? Thus, no federal 1065 required.

Hi Rick,

The IRS would consider the LLC a partnership despite the fact the husband and wife live in a community property State. They would look to the fact that two trusts (the husband’s IRA, and the wife’s IRA) are members of the LLC, and would require the LLC to file a 1065.

Hope this helps.

Jordan

My husband and I formed a joint Roth IRA LLC in 2012. We purchase debt and have a servicing company collect our payments. At the end of 2012, the servicing company issued a 1099 to our LLC which has its own EIN number. I do realize now that we need to file a partnership return. Once we receive our K-1 how do we let the IRS know that the interest is tax free/deferred on our personal reutrn? Or maybe we should issue the K-1 to the custodian of the IRA accounts? That would solve the issue of no taxes due on that amount. Also, when we give our custodian the end of the year value of all assets, should we include the exact figure that was on the 1099?

Hi Rosalie,

The 1065 return and the K-1s provide a space to list the partner(s) as IRAs. Technically, the partnership Roth IRA LLC would issue the K-1s to each of your Roth IRAs, because those two accounts are the owners of the LLC.

The valuation you provide to the Custodian should show the total current value of the LLC. You’d take into account all the assets of the LLC, and list the total value. Some Custodians ask for a list of the particular assets of the LLC with a current value for each asset, while others ask only for a total dollar amount. All Custodians have their own way of doing it, so you should probably check with them first.

Hi Jordan,

Thanks for these wonderful and detailed articles. This is the best informative source for IRA LLCs. Do not have question for now. Just want you to know I appreciate your efforts at helping others.

Once a multimember LLC is formed, can the percentages change?

Say my wife and I are 50/50, and start with a $150K joint investment in a property.

Years later, the LLC contains the property plus $50K. She needs to start RMDs sooner than I do. Do I take the same cash, say $10K that she takes a an RMD and move it to my regular IRA? Or does my ownership percent of LLC just creep up?

Hi Joe,

You ask a tricky question, because the answer depends a bit on how the LLC is internally structured. Generally it is advisable for the LLC to distribute funds back to each IRA pro rata, so that the percentages don’t change in the LLC. There is virtually no guidance on this specific issue either in the code or in anything the DOL or IRS has put out, so its best to be conservative here.

If this were an known issue going in, the LLC could possibly be structured to allow ownership fluctuation, but again, you’d be venturing into the unknown.

Hi Jordan,

Thanks for all your responses you provided regarding partnership LLC. I have two questions regarding EIN #.

While applying for a FED ID #, do you use the EIN # of the custodian and apply as a third party or you use the SSN number of the IRA owner?

In K-1 there are two places to mention the EIN number. A–>Partnership EIN number and E–>Partners Identifying number. Would E–> be the custodian’s EIN number?

Thanks,

Ven

There’s a terrific amount of knodgewle in this article!

Thanks for the informative article.

You mentioned a Multi member LLC files a K-1 to each owner/IRA.

In the case of an IRA owner – whose Tax identification number is used? The IRA does not have a typical Tax Id number if I understand correctly. So how would the CPA prepare the K-1?

Thanks,

Jordan,

I have funded an LLC with two IRAs, a traditional and a Roth. Both IRA’s are mine. Would I need to file a 1065 for this LLC?

Hi David,

There’s a good chance the LLC will need to file a 1065, although not necessarily; it depends on the situation.

I would suggest you talk with a CPA who’s familiar with these structures. If you don’t have one, I’ll be happy to recommend one we work with. Give us a call, or send me an email, and I’ll get his info over to you. My email is jordan [at] checkbookira dot com

My wife and I have funded an LLC with our IRAs (4 in all: 2 Traditional and 2 ROTH). Your description of how to handle the tax reporting for these have been very helpful and relevant to our situation. However, we have structured the LLC in Nevis with the LLC’s bank account in Belize for asset protection purposes.

What additional tax reporting requirements and forms come into play in this scenario.

This is our first tax year since creating this so this in new to us.

Thanks

Hi David,

To be honest, I don’t know the answer to that question. We have a lot of clients who live offshore, or have gone offshore with their retirement funds, but we work with a CPA in Colombia who handles that side of things for us. I’ll be happy to pass along his contact information. Give us a call if you’d like his info.

Hello,

I’ve gone through the website and there is some excellent information here. Something I can’t seem to figure out, although I think I already have the answer, is whether or not the LLC can have members that are not IRA’s. For example, could the LLC be owned by 25% by IRA-1, 25% by IRA-2, 25% by owner of IRA-1, and 25% by owner IRA-2? My guess is that this is ok, but I could be wrong. Please advise. Feel free to use any other type of ownership structure that is not 100% owned by an IRA. Thanks in advance.

Jon,

Its possible for an LLC or other entity to be owned by multiple iRAs, or a mixture of IRAs and personal money. The parties would need to be looked at the ensure they’re not prohibited parties, and some tax issues change with the entity once multiple parties come in as owners, because the entity is then treated as a partnership for tax purposes (doesn’t apply to corporations).

So sure, its fine. I’d suggest having an attorney look through everything to make sure you don’t have any prohibited transaction issues, and no surprises on the tax end of things.

Jordan,

This is an amazing wealth of information, thank you for all your insight.

I have funded my LLC with my single IRA funds, but my LLC was created with my wife as a member, and myself as manager. Would I need to file a 1065 for this LLC?

Hi Jordan,

My wife and I want to use 2 SDIRAs (or 1 SDIRA and cash) to buy a piece of raw land that we might later want to build on (a retirement home). She is 6 years older than I am, and the split of monies would be about 70/30 in her favor. So to use rough numbers, we buy a property for 100K and she puts in 70k from SDIRA, and I put in 30K either cash or a second SDIRA (preferably cash). SDIRA rules state that we cannot personally use a property that is owned by the SDIRA (that would be a prohibited activity). But if the SDIRAs (and cash) are “invested” in an LLC, and the LLC owns the raw land, how does that affect our ability to personally benefit from the land in the future? Do the SDIRA rules still apply? Or are there other rules from the LLC that would apply?

Also, if we used SDIRA and cash (without an LLC), would she have to take a distribution of the entire property (or it’s value) in order to then be able to build on (and live on) the property?

Thanks,

-Eric

Hi Eric,

What your wanting to do is far better done through a Solo 401(k) than a IRA LLC; but it can be done with an IRA LLC. You wouldn’t want to mix IRA funds and personal funds in an LLC though for a number of reasons.

Bottom line is that so long as the one IRA or both IRAs own any portion of the property, the property is going to be off-limits to both of you. Your wife can take an in-kind distribution of the property either in one fell-swoop, or she can distribute portions of the property to limit the tax liability. You wouldn’t be able to use the property until the IRA has divested 100% of it’s ownership in the property though.

As I mentioned above, you’re far better off doing this deal through a Solo 401(k). You’re able to mix monies within the 401(k) in ways that can’t be done with an IRA, and there are some interesting options for distributing the property from the 401(k) that are off the table in an IRA structure. Give us a call, and we’ll go over your situation.

I see many comments about buying “rental” property. My IRA buys distressed houses or land (15 to 20 a year) and then resells them within 6 to 12 months. We do not rent any property. We resell them “as is” and we do not do major repairs, only minor maintenance. I am retired and do not deal in property outside of my IRA. Is my ira in danger of the IRS classifying the capital gains from these resales as Unrelated business Income?

Hey Mickey,

There’s a chance those properties would be considered “inventory”, which probably would kick the profits over to UBIT. There’s a good CPA firm we work with who could take a look at your situation and give you their opinion on it. I’ll email you their info.

Howdy! I’ve learned several things here, thanks for the good info. I am trying to figure out if dissolving an IRA LLC is the right thing to do. Last fall, mother, brother and I set one up w/assistance of a property investment company (so we could invest with them) – they did the structure, 3 SDIRAs (2 Roth, 1 traditional), EIN and checkbook LLC account.

Investment ended this summer, with no viable follow-on offer. Now they’re not so helpful with LLC questions any more (go figure) and I am at odds on what to do. IRAs are FEE-ing us to death, so we need to move or close them. We closed out the checkbook account and sent proper proportions to each IRA, but custodian won’t close accounts or stop charging us the asset fees until we dissolve the LLC.

We probably don’t want to do another similar investment, but either brother and I or mother and I might want to do something, so I don’t know if there is a way to vote to change the LLC structure to two members? Or even one? We kinda created a monster and don’t know how to neutralize it. (At least now I know we need to file for last year!)

The best thing to do in my opinion is to go ahead and dissolve the LLC. The Custodian won’t close out the investment, because they want to see proof that the LLC is dissolve. As weird as this sounds, all Custodians require this, because they don’t want you using that LLC with personal funds for any sort of tax-evasion hanky panky. Not that you would do that, but I guess there are people out there who do.

Generally, a self-directed IRA Custodian will require a copy of the filed Articles of Dissolution (or the equivalent), and a closing bank statement, showing a $0 balance for the LLC’s checking account. Its also a good idea to send a letter to the IRS, informing them that the entity is dissolved, and ask them to close the EIN account on their books. If you don’t do that, they’ll come fishing around next year, asking why no 1065 partnership return was done.

If you need a hand with any of that, I’m happy to refer you to an attorney we work with.

Hello Jordan,

Great info thank you. I am considering creating a 50/50 jointed check book IRA form my wife and I to buy and sell properties and maybe some short term loans. I had a few questions I am hoping you maybe able to clarify.

1. Once we create the account as 50/50 ownership later on can I roll over another IRA/401k account I have into that existing check book IRA and adjust the partnership ownership percentage?

2. Does the percentage of ownership needs to be equal to the percentage of each party contribution to the check book IRA? Example Party one puts $25K and Party two puts $75K would the ownership have to be 25/75 or could it be 50/50 provided both parties are OK with this?

3. Other than the 1065 and K1 forms are there any other reporting items you would need to report the IRS or Custodian? Example Sales contracts for deals done? Contracts for loans? Parties information we have done transactions with?etc.

Thank you

William

Hi William,

Good questions here.

Before I answer them, I’ll say this – anytime a husband and wife are wanting to combine their retirement funds and in some way co-invest, they should absolutely look at getting into a Solo 401(k) before anything else. Combining funds in an IRA based structure can be done, but its tricky (as you’ll see below). The Solo 401(k), being an entirely different animal, allows you to do things you can’t even dream of doing with an IRA, and the ability to co-invest is seamless.

1. The honest answer here is – no one knows. Irregardless of what anyone says, there’s no guidance from case law here at all, so for now its a crap-shoot on this question. My default position is that, until there’s a court case on the books saying otherwise, no additional funds should come into the LLC after the initial capital contributions from either IRA.

2. The percentages would need to follow the capital contributions, or rather, be based on those initial contributions. To base it on anything else would be to favor one account over the other, and shift value from one account to the other, which would definitely be a PT (prohibited transaction).

3. The IRS doesn’t collect any specific information on retirement accounts other than the Form 5498 filed by the Custodians at the end of the year. Even on a plain-jane stock IRA with a brokerage firm, the IRS never sees what the IRA invests in, only the changing dollar value of the account from year to year. Any contracts, closing docs, promissory notes, etc. related to the deals the LLC does, are all entirely private and aren’t filed with anyone. You’d keep those in your files in case the LLC was ever audited.

Let me know if you want to go through a few things on the Solo 401(k) to see if that would be a viable option for you.

Hi Jordan,

My wife and I are considering using our IRA’s to make a loan to our church to purchase a building. We have 4 separate accounts. I have a traditional IRA from a former job, a simple IRA from my current job, and a Roth IRA. My wife has a SEP IRA from a previous job. All of the IRA’a are currently invested with Vanguard in various funds. My questions are as follows.

1. Are there any prohibited transaction issues involved with making loans to a church of which you are a member?

2. From an IRS reporting angle, would it make more sense to create 4 separate Checkbook IRA’s that make 4 separate loans to the church rather than forming an LLC funded by all 4 accounts that makes a single loan.

3. If the Accounts are kept separate making 4 separate loans, can I use a higher interest rate for the Roth? For instance, if I was aiming for an overall percentage rate of 4% could I have the 3 Traditional IRAs make loans at 1% and the Roth make a loan at 13% so that the same amount of total interest is earned but a larger percentage of it is going to the tax free account. Would this raise red flags with the IRS as transferring wealth from one account to the other or would this be permissible since technically there is no legal relationship between the different accounts?

Hey Matt,

I’ve sent you an email, so we can talk about this at greater length. Using an IRA LLC may not be the best thing in your case, but we can talk about it.

We have 3 partners and looking to invest in a parcel of land for future construction project. We are not looking to built but to flip the approved site to a developer. The ownership of a land is by an LLC. Can I invest in this project through Roth IRA LLC for my 33% share?

Hi Boris,

Yes, you can probably do that, so long as the other partners are not prohibited parties to the IRA, and neither is the developer. You might have to worry about UBIT, given that it’s a flip, and if there’s any debt on the property then you’ll have UDFI to contend with. You would need to be hands-off with the investment though; if any other work is needed by the land-owning LLC, you could not do it.