IRS Filing Requirements for a CheckBook IRA LLC

This post addresses tax filing requirements for CheckBook IRA structures that have one IRA and one LLC, which is to say single-member LLCs. We explain tax reporting for multi-member IRA LLCs in this post.

Please also note that this article assumes the IRA LLC has not incurred UBTI (Unrelated Business Taxable Income). Also, check out our NEW Solo 401(k), for some it’s a lot better.

THE BOTTOM LINE:

There are no Federal filing requirements for a single-member IRA LLC. There. That was easy wasn’t it?

It’s pretty straightforward once you get through it, but I’ve found that this is a subject that can cause a lot of confusion. When you take a self-directed IRA and throw in an LLC to boot, most people will scratch their heads and wonder, “I know this thing has to file with somebody at some point, but what does it file and with whom?”

While a single-member IRA LLC never files a standalone tax return, the income does need to be reported. If you want to know who does that and how – read on.

Why a Solo 401(k) is Better than an IRA/LLC

- No custodian

- Use leverage with no tax

- Spouses can share

- Contribute up to $58,000

- Borrow up to $50,000 personally

- Less expensive

- Buy ANY type of metals

C-Corporations, Partnerships & LLCs

C-Corporations

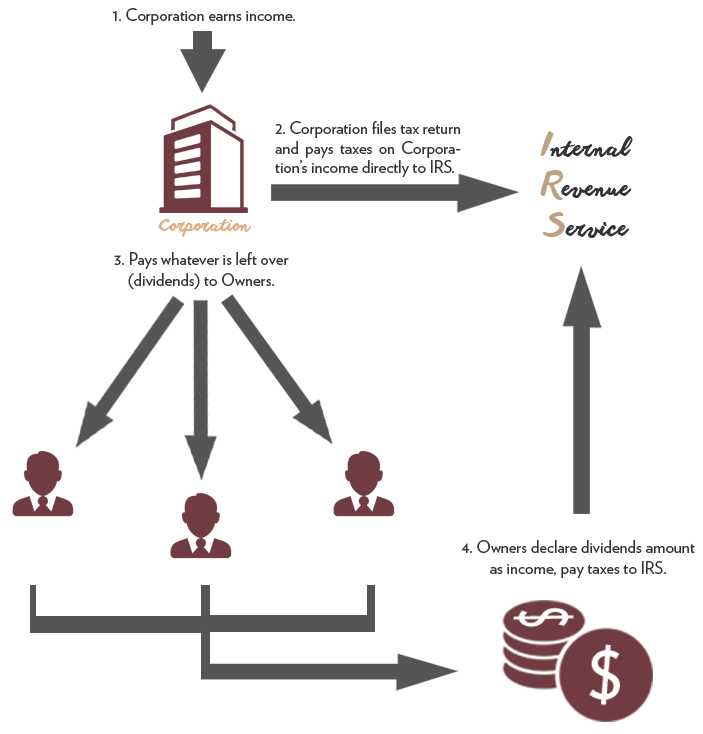

A C-Corporation (C-Corp) is an entity which issues stock to its owners, and pays the profits of the corporation to its owners each year by way of sending out dividends. A C-Corp is taxed separately from its owners, which is to say that the C-Corp itself files a tax return and pays tax on the income earned by the company. Whatever is left over after taxation at the corporate level is then paid out to the owners of the C-Corp; these payments are called dividends. The owners must then declare those dividends as taxable income and pay taxes on those dividends again. You will commonly hear this referred to as “double taxation”. The C-Corp is taxed at the corporate level, and then the dividends are taxed at the individual level.

Partnerships

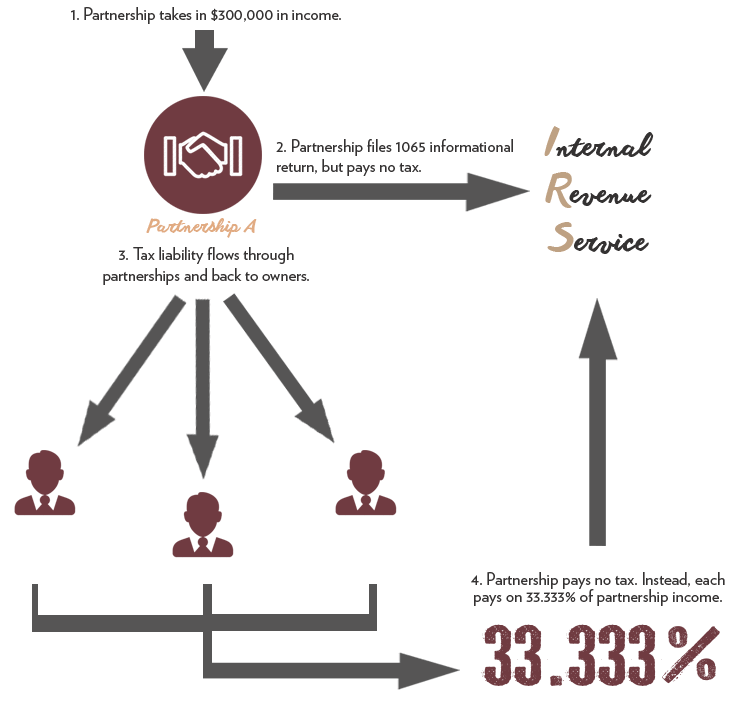

A Partnership may take a number of different forms, but unlike a C-Corp, a partnership pays no tax. A partnership is considered a flow-through entity which means that the partnership itself is not taxed, only the individuals who own the partnership. If Partnership A were owned by three brothers, all with an equal share, and if the partnership were to make $300,000 in year 2011, the partnership would pay no tax on it’s income. Instead, each partner or owner would have to pay tax on the amount of income that their share of the partnership earned. In this case, each brother owns 33.333%. Since the partnership made $300,000, each brother would then have to declare $100,000 (33.333% of $300,000) as income and pay tax on that amount.

Limited Liability Companies (LLC)

Limited Liability Companies are interesting entities because they combine the best parts of a C-Corp and a Partnership. The LLC enjoys the asset protection of a C-Corp, while retaining the flow-through tax treatment of a Partnership.

LLCs are not recognized by the IRS as taxable entities, so an LLC must make an election on how it wants to be taxed. An LLC can be taxed as a Corporation, Partnership, or it can be disregarded as an entity separate from its owner. (A tax return would be required of the LLC should it elect to be taxed as a corporation. That subject, however, is beyond the scope of this article as an IRA LLC should never choose to be taxed as a corporation.)

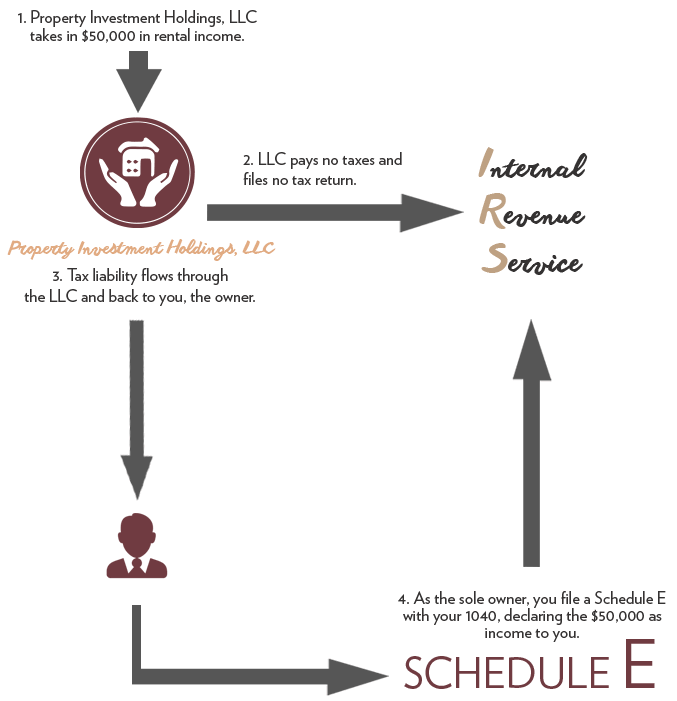

In the case of a single-member IRA LLC, the IRS would automatically classify the company as a “disregarded entity”. This means that the Service disregards the LLC for Federal tax filings, and requires that the income of the company be reported on the owner’s tax return. Any tax that is due would be paid by the owner; the LLC itself does not pay any taxes. Or to put it another way, the income of the LLC becomes the income of the owner, who is ultimately responsible for paying taxes on that income.

Here’s an example using you, personally:

You own 100% of Property Investment Holdings, LLC, which means it is a single-member LLC. The company owns several rental properties, and takes in $50,000 in rental income throughout the year. The LLC itself pays no tax, nor does it file a tax return. Instead, the tax liability of that $50,000 flows through Property Investment Holdings, LLC and back to you as the sole owner. You must then declare that $50,000 as income on Schedule E of your 1040 and pay tax on the declared amount.

Filing Requirements for a CheckBook IRA LLC

Now that you understand the basics of how tax liability passes through a single-member LLC and back to it’s owner, let’s look at how this fits in when you’re dealing with a CheckBook IRA. If all of this is new to you, we deal with the IRA LLC structure in more detail here.

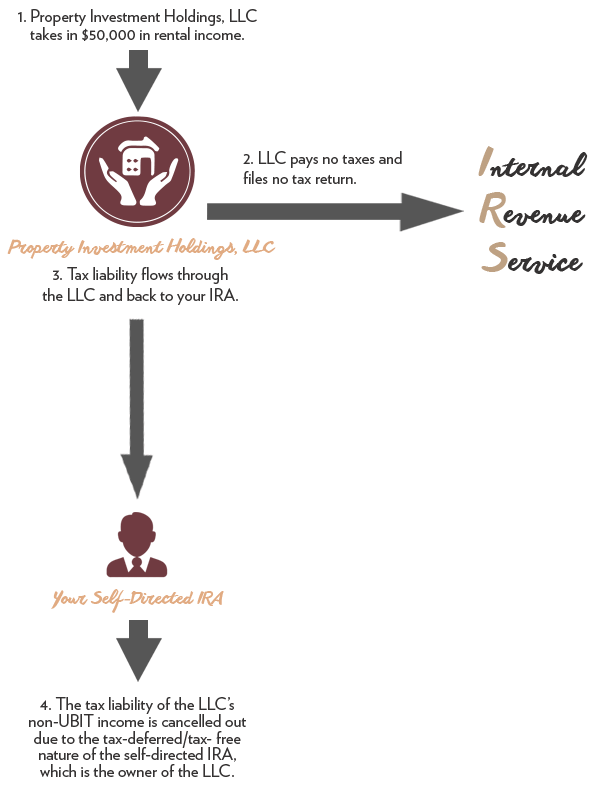

We used an example above where you personally owned an LLC named Property Investment Holdings, which made $50,000 in rental income. Let’s take that example, and simply replace the names and figures:

In this chart, you can see that everything is the same except for the owner. The owner is your IRA. Property Investment Holdings, LLC, which is owned wholly by your IRA, takes in $50,000 in rental income. The LLC pays no tax, neither does it file a return, but passes the tax liability up to it’s owner. The IRA is then responsible for paying any taxes on this income. However, because of the tax free/tax deferred nature of the IRA, and because the income is rental income and is therefore not subject to Unrelated Business Income Tax, no tax is due on the $50,000 that Property Investment Holdings, LLC earned.

But what about reporting? Since the LLC pays no tax, and is disregarded by the IRS for filing purposes, who reports the income? Answer: the owner, which in this case is your IRA. Even though no tax is due, it must be reported that your IRA’s value increased by $50,000.

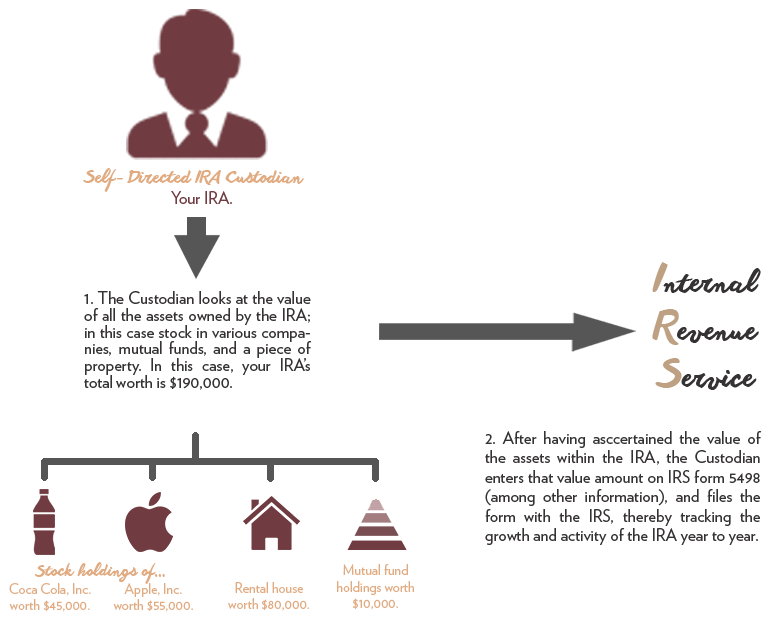

IRS Form 5498: The IRA’s Tax Return (sort of)

Each year, every self-directed IRA Custodian must file IRS form 5498 for every IRA it oversees. This form is an informational filing which tracks a number of things like how much was contributed to the account over the course of the year, any rollovers, distributions, etc… It is essentially a form which is filed to track the value of your IRA each year. The Custodian collects the information on your IRA, completes the form, and files it with the IRS. (Keep in mind that an IRA can incur taxable income and actually owe taxes. In that case a 990T return would need to be filed for the IRA to figure the taxable income and taxes due.)

In order for the Custodian to accurately report the value of your IRA, they must collect information on the value of the assets within your account. Let’s look at an example:

In this case, your IRA owns a rental house, stock in Apple, Inc., stock in Coca-Cola, Inc., and also holds some mutual funds. The Custodian will look to the value of each asset to determine the total worth of your IRA. Once they have the total value, they enter it on form 5498, and that’s the end of that.

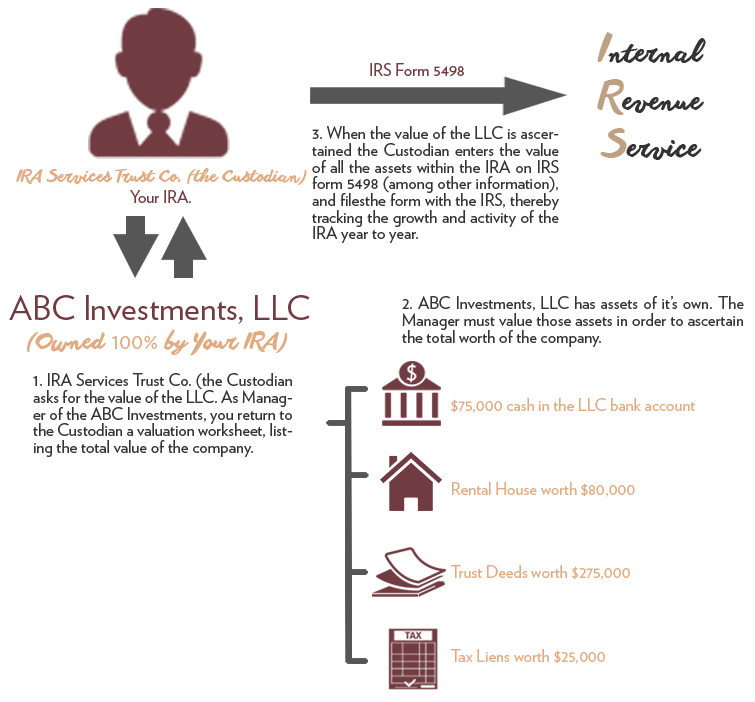

Now let’s look at what happens when you have a CheckBook IRA LLC:

We work with different Qualified custodians, but we search for the best ones for price and customer service. Each year they send out a request that an IRA LLC Valuation Worksheet be filled out and returned to them. You can see that the only asset your IRA owns is the LLC. Unlike, say Apple, Inc., whose share price is immediately available because those shares are traded and valued publicly, the LLC is a private company. As such, the LLC’s worth is not readily apparent. As you can see in the chart, the LLC owns assets of its own, and as the Manager, you would need to figure out the value of those assets in order to arrive at the LLC’s total worth. Once the Custodian receives the valuation worksheet, they will have the information they need to complete form 5498. Pretty simple.

While the tax reporting issues are straightforward and relatively easy (especially with a single-member IRA LLC), it is important to understand what is expected of you. This article was intended to give you a basic foundation of the reporting requirements. Obviously you should consult with an experienced tax professional, especially if you’ve incurred UBIT or UDFI taxable income.

Feel free to chime in with questions or comments.

In the last diagram, if ABC Investments LLC together with another IRA LLC (XYZ Investments LLC) were to form a holding company ABC-XYZ Holdings, LLC, would either IRA owner be allowed to work for the holding company without violating self-dealing or conflict of interest rules?

Hi Wilbur,

ABC Investments, LLC and another IRA LLC could certainly form a holding company (provided that the IRA owner of the other IRA LLC is not a prohibited party). Certainly either or both, IRA owners could serve as unpaid Manager(s) of ABC-XYZ Holdings, LLC. But, when you ask if either IRA owner could “work for” the holding company, do you mean as paid employees, receiving W-2 income? If that’s what you’re asking, then the answer depends on the situation.

It would depend on the original intent of the transaction, and also the ownership each IRA LLC holds in ABC-XYZ Holdings. Do you have any specifics regarding the proposed transaction? If you have something specific in mind, I’d be happy to go through it with you and make sure everything is above board. You can contact me directly at [email protected] or 1-800-482-2760.

Thank you for this article. I’ve never been able to get a straight answer from anyone when it comes to this sort of thing. Even my CPA was telling me the LLC has to file a tax return.

You mention doing a article on fliling requirements for partnerships. Have you done that yet, and if not, when will you?

Thanks again,

Bill W.

Hi Bill,

Thanks for the compliment! I’m glad you found the article helpful. Most CPAs are just unfamiliar with the structure, and so sometimes end up making recommendations that don’t make any sense. I thought a post like this would benefit our current clients, prospective clients, and others with IRA LLCs who haven’t been able to find an answer to what is required of the LLC each year.

I haven’t published the partnership filing requirements post yet, but I plan to sometime next week.

Other than setup and yearly one time fee’s, what other charges might I incurr with the custodian in an llc checkbook ira?

Thanks for your question, Jim.

Once the setup is complete, IRA Services will charge your IRA an annual account fee of $75, and also a $10 per quarter asset fee (the asset being the LLC), for a total of $115. The IRA could incur other fees going forward though, depending on your situation. Generally, anytime the IRA takes any action at all, the Custodian will charge you for it. The LLC itself of course, will never incur any Custodial fees.

So, if you set up the IRA LLC structure, and your IRA takes no more action, you would only have the $115 yearly charge. To give you an example of how additional fees could be incurred, let’s say you have an IRA LLC, and let’s say you want to make a contribution to your IRA and then move those funds into the LLC. You would make the contribution as you normally would by sending a check or bank wire to the Custodian to be deposited in your account. You would then instruct the Custodian to invest the contribution amount into the LLC. Since your IRA is adding additional funds to the LLC, the Custodian would treat that as a transaction and would charge a transaction fee, and a delivery fee for a check or bank wire. In IRA Services’ case, it would total $45-60.

Even though it is possible to incur extra IRA fees each year, those fees are still very low. Feel free to contact us if you have additional questions, or if you’d like us to review your situation to identify exactly what you would be paying each year. You can reach us at (800) 783-6409 or you can contact me directly at 1-800-482-2760 or [email protected].

What about when I turn 59 1/2? To take a distribution, do I have to take it as a transaction from the custodian or write myself a check from the LLC.

Jim,

Good question. You wouldn’t be able to take a distribution directly from the LLC. Any distribution would need to come from the IRA itself. I published a post a few days ago detailing this process.

The title of the post is Making a Distribution with the CheckBook IRA LLC

Let me know if you have any other questions.

What happens if there are 2 IRAs (my wife and mine) that invest in the LLC and therefore would not be a single owner IRA. My understanding is that the IRA would then need to file a tax return. Would it be subject to taxes? I dont want to pay taxes from my IRA funds.

Hi Alan,

I’ll be posting an article next week sometime, detailing the filing requirements of a multi-member IRA LLC. In the meantime, I hope this response answers your question.

In the scenario you lay out, the LLC would be treated as a partnership by the IRS. The partnership would not be taxed, but would retain it’s flow-through nature. The LLC would however, be required to file a 1065 partnership return (which is an informational filing), and complete K-1 income statements for the owners, which in this case would be the two IRAs.

So the LLC, even though it has multiple owners, would not pay taxes, but would pass the tax liability back up to it’s owners just like in the diagram(s) above. The only difference would be that, because the LLC has multiple owners it would be considered a partnership, the LLC would need to file the 1065 return and K-1s to the owners.

Jordan, have you written your article on the filing requirements of a multi-member IRA LLC?

Also is there a simple step by step instruction for completing form 1065?

Arthur,

I’ve written the multi-member IRA LLC article, and am just putting the finishing touches on the charts. Hopefully I’ll have it up in the next few days.

Here is a good place to start on the 1065 Partnership return. This site gives detailed instructions and explanations for each part of the return, including the Schedule K-1.

Best of luck!

Hi Jordan,

Thank you for your post. As a tax attorney who has worked with thousands of self-directed IRA investors, I appreciate the simplicity of your diagrams. My one comment relates to when you transition from discussing a single-member lawn mower service, which is owned by an individual, to a single-member IRA/LLC. Although you are correct that IRA and LLC tax filings are very minimal in most single-member IRA/LLC situations, if the $50,000 of income earned by the IRA/LLC is of a character that is not exempt from “unrelated business taxable income”, the IRA will need to file a tax return (Form 990T) and pay a tax. For example, ABC Investments, LLC invests into a lawn mowing business – or a more common example – debt-financed real estate, the IRA could face significant tax problems if the IRA does not file Form 990T. Further, because IRA Services Trust Company (along with every other IRA/LLC custodian) will defer responsibility for filing the 990T – which makes perfect sense because the custodian is not in a position to know when the filing requirement is triggered – the IRA owner will be responsible for recognizing when this situation arises.

Hi Warren,

Thanks for the comment. You are exactly correct. I was planning on doing a separate post for situations in which UBIT might arise, as figuring out how to pay tax on UBIT and what to file tends to be an area of confusion for most people with IRA LLCs. Thanks for beating me to it 🙂

For a debt financed rental real estate situation UBTI would not be a concern since the income is rent. Is that true?

However, since it includes debt (financing) there is a possibility that UDFI come into play. However, in a normal 80/20 Loan/Downpayment scenario, the net income is very low sometimes negative when depreciation is involved. If no net income is realized is UDFI a concern?

The debt-finance tax applies to any income the property produces, irregardless of the form of the income. Rents, lease income, profits from the sale of the property – all these would result in income and part of that would be taxed.

The tax is applied to the portion of the income that was financed, so using your example, if the property were 80% financed, which is highly unlikely as all loans to an IRA LLC have to be on a non-recourse basis and so generally banks won’t loan more than about 50%, but using your example of 80% financing, 80% of the net rental or lease income would be subject to tax. If the LLC ends up in a zero tax situation because of low rents and the net comes out to zero or negative, the no tax would be due, because there’s no income to tax. However, any time the property produces a positive income, then tax would be due.

When the debt is reduced to zero, then the tax issues go out the window because there is no debt on the property.

Thank you Warren and Jordan, my accountant thought the 990T was only for charitable orgs. I incurred UBIT this year for the first time in my Roth IRA LLC and we are trying to figure this all out.

Hey Gail,

Its funny how a lot of CPAs don’t realize IRAs are Trusts, and file the 990-T if tax is due. I’m glad my email to your CPA helped with his confusion.

I am a sole owner of an IRA LCC that owns rental properties. at the end of the the year I have to establish the value of each property. Values will vary from year to year and using the services of an appraiser is cost prohibitive…what is the accepted standard to establish value.

I have used the Zillow as many banks do but would like to find out what your answer is.

Thank you

Hi Danielle,

The accepted standard to establish value depends on the Custodian you’re working with. Some Custodians require that each asset of the LLC be independently appraised, while others will accept a value for the LLC without a formal appraisal. Many Custodians do not require a formal appraisal/valuation of the LLC until the client reaches the age of 70 1/2 and must begin taking minimum distributions. At that point, being specific about the value of the IRA becomes more important, because of the fact that the minimum distribution amount is based on the value of the IRA.

I would suggest you talk directly with your Custodian to find out what their accepted method of valuing the LLC is, so that you can decide how to meet their requirements cost-effectively.

I just found out about your company from a webinar I was watching. I am a little confused after leaving my accountants office. I am a sole proprietor of a very, very small business and looking to flip properties and possibly purchase Tax Lien certificates and / or Tax deeds using my IRA money. He told me I didn’t need to be an LLC. I told him I have a self directed IRA but was trying to find out about getting it to be a checkbook IRA to use for the purchases. I am mid 60’s, disabled and want to put all profits back into the self directed IRA as long as I can. Originally I was going to try to link my bank account with my IRA mutual account company but if I did that I would only be able to contribute $6k annually I was told. Can your company set up or tell me how to go about getting started and meeting my goals? Thank You

Hi Frank,

I think it’s best that you call our office. We’ll be able to go into as much detail as you would like regarding your situation and how we might be able to help. You can reach us at 1-800-482-2760.

Jordan,

What are the rules for placing structures such as mobile homes or movable stuctures on personally owned property to rent as a bed and breakfast / hunting and fishing lodge. Income would be divided as lodging and fishing / hunting. The lodging would go to the IRA-LLC and the fishing / hunting would go to my farm.

Hunting and fishing with lodging would be an income creator for the LLC; however, I know this must be arms length and for the IRA’s benefit and not my personal benefit.

I would like to include the hunting and or fishing income as a deposit into the IRA.

Would the issue of the personal property be self dealing with no lease? I would not charge any fees for the land use as I have never charged anyone for hunting or fishing. This is very confusing and complicated to me. I would like to place enough property into the IRA-LLC for the movable stuctures but I do not think this is possible.

Also the business plan would have the business for the benefit of the IRA-LLC, the personal property would be a BIG RED FLAG!

Any suggestions regarding this business plan.

I do not want to violate the rules.

Hi Joseph,

The transaction you describe would be considered prohibited by the IRS, unfortunately. There’s really no way it could be done, considering the property in question is owned by you.

No transaction of any kind can occur between the IRA LLC and you or any other prohibited party. So, the IRA LLC could not rent or lease the land from you. Now, you’re smart to point out that you would want the benefit to go to the IRA LLC, but unfortunately the IRS is ahead of you on that as well. 26 USC § 4975(1)(D) states that any deal that the IRA does cannot benefit a prohibited party (you). So if you were to simply give the land to the IRA LLC, or let the IRA LLC use the property without charging the company any rent, the IRS would still consider that a transaction between you and the LLC.

I wrote a four-part series on prohibited transactions that goes through much of the nitty gritty regarding these rules. It might be helpful to read through them. Here’s the first part: Prohibited Transaction Rules, Part I: An IRA LLC Primer

The bottom line is that the IRA LLC could not use, rent, purchase, or lease your own personal land, because it is your property and you are prohibited from dealing with the LLC in any way.

As a side note, the income produced from a transaction like this would most likely be considered business income and would taxed according to the UBIT rules.

If this land belonged to a friend of yours or a neighbor or something, there are several ways you could structure this so that it would be legal, and non-taxable. Because the property is owned by you though, unfortunately you’re cut off at the knees; there just isn’t a way to do it legally.

If you have other options available, I’ll be happy to review them and see if anything can be done within the law. Feel free to call us at 1-800-482-2760 or email me at [email protected]

Couldn’t he sell the land to non-disqualified party, the repurchase it using the IRA or IRA LLC, then do what he wants? He might have to subdivide out the portion he wants to live on before selling.

A qualified buyer might be his sister, brother, or sister/brother inlaws. It could also be a trustworthy neighbor.

The IRS would consider selling the property to a non-disqualified party and then buying the property with personal funds, to be a structured transaction, and a prohibited transaction. They would look past the fact that it was bought by a non-disqualified party, and claim your original intent was to use the third party for the sole purpose of removing the property from the IRA and putting it in your own name. It sounds good on paper, but in reality, it would result in a prohibited transaction.

Hi Jordon,

Your site as been helpful for answering questions about the Checkbook IRA. Can you tell me what requirements there are for state filing and does your company help with these forms also.

Hi Mary,

Thanks for the question. Yearly filing requirements vary from State to State. Some States require an annual report be filed each year, some States don’t require any filing, and some States impose a franchise tax on the LLC which necessitates a franchise tax report be filed each year. If filings are needed, your CPA should have no problem doing it for you.

How is being the manager of the LLC not considered providing services to the IRA? It is my understanding that a single-member LLC is deemed to be disregarded for income tax purposes (thus no annual tax return is required) and is therefore treated as if it didn’t exist. So if you are a manager of something that doesn’t exist and are writing checks basically on behalf of the IRA itself, how is that not a prohibited transaction??

Thanks for the comment, Jack.

We’ve written on this subject in more length on our page “Is It Legal?”; I’ve laid out the legal history of the CheckBook IRA concept on that page..

To summarize: if the IRA owner chooses to manage the LLC, he is considered a fiduciary to the plan as mentioned in 26 USC, 4975(e)(2)(A) and defined in 4975(e)(3), which is to say he is a party that has authority over the assets of the plan.

The code says that a fiduciary is a disqualified person because of the authority he has over the plan assets. As a result, the fiduciary cannot deal with the plan assets for his own benefit. Simply being present as a fiduciary and directing the investments of the LLC is not itself a prohibited transaction. We know this from Swanson v. Commissioner and FSA 200128011. There must be a requisite transaction between the fiduciary and the plan for the benefit of the fiduciary, his spouse, and/or his lineal descendants and their spouses.

Think of it this way: if you had an IRA, and secured the services of a financial advisor who directed the investments of your IRA, and had authority over the funds within that IRA – that advisor would be a “fiduciary” to the plan, and would be considered a “disqualified person”. As a result, he would not be able to deal with the assets of your IRA for his own benefit. Yet, no one would dispute that he could continue to direct the investments of the IRA, so long as he stayed within the prohibited transaction rules set forth in 4975. To say otherwise would be to say that every financial advisor in the country is guilty of entering into prohibited transactions on a daily basis.

The finding of the court in the Swanson case sheds some light on this subject. When the Service argued that Mr. Swanson, as Director of the corporation his IRA had bought, had entered into a prohibited transaction when he caused dividend payments to be paid back to his IRA, the court replied that a prohibited transaction did not occur because Mr. Swanson, even though he was a fiduciary, did not deal with the assets of the plan in his own benefit.

The Department of Labor has confirmed this in a number of advisory opinion letters. The DOL has sole authority to interpret what is a prohibited transaction, and the IRS is bound by those interpretations.

As regards your question about the LLC being disregarded – the IRS disregards the LLC for tax filing purposes only. That has nothing to do with the corpus of the LLC itself. The LLC still exists, and is still an entity separate from its owner; its just that for purposes of taxation, the IRS does not recognize LLCs as being taxable entities, so they treat them differently than Corporations or Trusts.

If you have any other questions, I’ll be happy to answer them. Feel free to contact us directly as well.

In regards to the multiple-owner [husband and wife] CheckbookIRA, you indicated earlier that the LLC would not incur any income taxes, but it would still be required to file under the partnership reporting requirements, Form 1065 and Schedule K-1 for each IRA member. What level of detail and how complex is the partnership reporting requirements for the IRA LLC?

Hi Steve,

The partnership return for a multi-member (husband & wife) IRA LLC would be completed like any other multi-member LLC. If a CPA is familiar with the 1065 return and K-1s, he/she will be able to complete the return for a multi-member IRA LLC.

Dear Checkbook IRA,

How is the annual valuation handeled if the capitol in a checkbook IRA LLC, comes from two different IRA’s,, for example from my and my wifes which is the case for our checkbook IRA LLC of which I am the managing director…it seems that the annual valuation form for each of the two contributing IRA’s should be done proportionally to the original capital investment from each IRA..is this correct..for example, My IRA contributed approximately 50K and My wifes 25K to the LLC which then purchased a property for 75K . this property was a forclosure which was rehabed and is now rented out. The current market value is about 150K, plus some annual rent income. Do I report valuation proportional to the original investment to each IRA? For example 1/3 x 150 for my wife and 2/3 x 150k for my IRA? Please let me know your thoughts.

Mr. Schmidt,

You’re correct that the valuation should be figured based on the proportional ownership of each IRA. If the ownership split is 33.333% and 66.666%, then each IRA owns that percentage of the total assets of the LLC.

I have a self direct IRA LLC structure set up already. I have to file the 990-T due to the debt financed property income. I would like to run a fiscal year end of June rather than a calender year end. Is this OK??? I haven’t filed anything yet with the IRS.

Hi Jason,

The fiscal year end of the LLC will depend on what was entered when you secured the EIN or Tax ID for the company. Generally, the IRS will default to December 31st. Assuming that the fiscal year end of the LLC is in fact December 31st, you’ll need to file the 990T according to that schedule for now.

When an EIN or Tax ID number is secured for an LLC or other entity, that information is not set in stone. Most people are unaware that an EIN account is opened with the IRS in the name of the entity. That account stays open until the Service receives word that the entity has been dissolved and the EIN is no longer needed. As a result, you can change the information and elections on file with the IRS. You must do this in writing, and its important to point out that you DO NOT change the information by filing a new SS4. Instead, you must submit the changes in writing to one of the Service’s offices.

You should submit a letter on the LLCs letterhead, and provide the assigned EIN, mailing address, State of organization, and Manager contact information. List the changes that should be made, and sign it as Manager. The IRS provides information on where to send the letter on their website. You can either mail it, or fax it to the address or fax number listed on the page. Remember that you are not to submit a new SS4 (even though it says the contact information is for filing an SS4), but a letter detailing the changes to the EIN account.

Finally, you can visit the IRS’ EIN help page, and refer to the question “What if I need to make changes to the information I submitted?”. You will see they require you do so in writing, and refer you to the contact page I linked to above.

Good Luck!

I just filed online for my tax id number for an LLC as corporation for tax purposes, is it too late to open a self directed IRA that will own this company? If not, what are the costs to change the owner info for the LLC?

Its probably best to leave the existing LLC alone, and form a new one for the Self-Directed IRA.

If you want to change the information that was given to the IRS on the SS4 or the online application, you can do so by submitting a written request to the Service that certain changes be made to the EIN account; the IRS does not charge you to make these changes.

Thank you Jordan! This information is very helpful. I wish I had seen this article before I filed for the EIN number. I would like to keep the same name of the LLC, so I will send a letter changing the name. I didn’t realize I had to open the IRA before filing for the EIN to get the LLC.

Again, Thank you! Great article!!!

I have recently set up a Checkbook IRA and rented out a property through a broker. They asked me to complete a W9 to report the rental income they had sent. I assume in filing out the W9, I would check the box for LLC and mark as Disregarded entity. Is there anything else I should be aware of when filling out W9?

Gary,

The company who set you up should be able to tell you how the W9 should be completed. Generally the IRA information is listed, as the IRA is the entity which pays any tax the LLC may incur. I don’t know the particulars of your situation, so its probably best to contact the company/attorney who set you up and review the form with them.

Hello Jordan,

thank you for the informative article and graphics.

I just went through the valuation for my single member IRA LLC.

I understand what you mean with: “There are no Federal filing requirements for a single-member IRA LLC.”

What about reporting taxes to the revenue services at the state level – do they simply follow the federal level and that’s it?

I my case, my IRA LLC was formed in AZ and looking at the ‘ARIZONA CORPORATE TAX RULING CTR 97-2’ document it says on page 3: “If a single member limited liability company is disregarded as an entity separate from its owner for federal income tax purposes, the limited liability company’s income will be included in the Arizona tax return of its owner.”

However the owner in this case is the IRA and doesn’t actually file an AZ tax return.

I guess putting all the information together I would also arrived at the conclusion that there is also no filing requirement on the state level (at least in AZ).

Can you please briefly comment on if that reasoning is sound?

Thank you,

Peter

Good question, Peter.

To be succinct, you are correct in your reasoning. Arizona is one of those wonderful States that does not require annual reporting on the LLC. Much like the Feds, most States don’t recognize LLC as taxable entities, and will generally only charge the LLC some sort of report or renewal fee. Some States like Cali, Texas, Alabama, and Tennessee impose a franchise tax on the LLC, but that’s a different animal from what you’re dealing with in Arizona.

Your IRA will not incur any income taxes at the State level, and so the LLC is only subject to Arizona’s annual filing requirements for LLCs, which thankfully is nothing.

Cheers!

Hi Jordan,

I am self filing my self directed IRA LLC in California.

I am reporting my debt financed income on the federal 990T.

Would I also report that on the California 109?

For the LLC do I need to file the California 568 as well?

I would need to also file the 5498 since I am the cusodial Agent correct?

Thanks, Jason

Jason,

If the IRA LLC has incurred debt-financed income, then you are right to complete the 990T return to calculate the IRA taxable income for the year. The reports to California will be related to the State’s franchise tax fee that is imposed against the LLC each year. I’m not intimately familiar with Cali’s franchise tax return, so I don’t want to lead you down the wrong road on that subject.

What I can tell you is that the State doesn’t care that the owner of the LLC is an IRA; every single-member LLC which is disregarded for Federal filing purposes, must complete the 568 and pay the minimum $800 franchise tax fee; that fee may go up depending on the amount of income the LLC generates. To my knowledge, a FTB109 would not be required for the LLC.

Form 5498 will be filed by the Custodian of your IRA, not by you. It is your responsibility to provide the Custodian with the year-end value of the LLC, so that the Custodian may figure the total worth of the IRA and report the value of your account on form 5498.

I hope this helps.

Jason,

I am interested in forming a IRA owned LLC for the purpose of loaning money secured by mortgages (hard money lending). Does it matter if the IRA is a standard IRA or Roth (I can’t see why that would matter)?

Is there a conflict with the “rules” If I am involved in the actual review of who and what property I make loans to? Property inspections or attending closings etc?

Last question: I am married and was wondering if there is a substantial disadvantage to having both my wife and I as LLC owners beyond the fact we need to file an information type return from the LLC?

It was nice talking with you this afternoon, Stephan. I hope I answered all of your questions. If you have any more, please let me know.

Jordan

Hi, your website is the most understandable informative website on the checkbook ira on the web! thanks!

Have you posted a entry yet on tax filings for multi-member IRA LLC?

I have one IRA LLC for my Roth IRA and my SEP IRA. I believe this makes it a multi member LLC.

I am little confused about how I actually document what percentage of the LLC is owned by the SEP vs Roth. Do I need to actually file a document somewhere detailing this?

Matt,

Thanks for the compliment 🙂

The company that set you up with the Roth & SEP IRA LLC, should have provided a place in the subscription agreement to show what percentage is owned by each IRA. This is a question you should direct to the company that set you up, but the funds put into LLC by each IRA (member capital contributions) will determine what the ownership interest of each IRA is, so long as no additional funds have been added to the LLC by either IRA.

The ownership breakdown should be detailed in the Subscription Agreement, which should accompany the Operating Agreement of the LLC. As this is a private agreement between the owners (the SEP & Roth), and the Manager, you do not need to file the agreement with anyone; it is private.

Dear Sir,

Thanks for the article! I see that you don’t recommend that an IRA LLC elect to pat taxes as a corporation. As luck would have it, I live in rip-off California, where they nail LLC holders tor an $800 registration fee, at a minimum!! The only thing I want to do is convert some of the cash in my IRA into precious metals…..and $800 seems like a lot of dough for the “privilege”! So maybe getting taxed as a corporation isn’t too bad an idea? Please let me know what you think. Thanks very much!

Hello Earl,

I know what you mean about California. Its amazing to me how the State can be so anti-business, and then be surprised when everyone runs away to friendlier climes.

I would not suggest the LLC be taxed as a corporation, partly because it would still be responsible for paying the $800 minimum franchise tax in California, but also because it would have to pay federal taxes as well. Its best to keep the LLC as a single-member disregarded entity to take advantage of the IRA’s ability to cancel out what would otherwise be taxable income. Having said that, you do have some other options when it comes to California. I’d be happy to go over them with you. You can contact me via email jordan[at]www.checkbookira.com or call us at 1-800-482-2760.

Jordon

It is obvious the intent is to make money for your IRA but sometimes things do not turn out as planned. Where would you be with the IRS if due to a bad investment your LLC lost money one year. Would that send up a red flag? Look how many people do lose money in there investments do to unforeseen circumstances.

Hi Mark,

You’re right that investments don’t always turn out as planned. If the LLC were to lose money on an investment, the year end valuation of the company would just be lower. As far as raising any red flags, the only way it would raise a flag in my opinion would be if the value was obnoxiously lower. For example, if an IRA was worth $500,000 in 2011, but then turned in a valuation of $45,000 in 2012 without any accompanying distributions to account for the loss of funds, the Service might sit up and take notice. If that were to happen, the most important thing would be that the Manager of the LLC must be able to show that the loss was legitimate, and not due to any funny-business. The IRS does not want people using these structures as a tax shelter, or as a way to use the funds personally without paying taxes. So long as the loss was legitimate, there would be no issues to worry about.

Have you done a post for IRS filings for multi-member LLC? I can’t find it on the website – just a mention that is will be in an upcoming blog.

Hi Winnie,

I had the multi-member post scheduled to go up at 3am this morning for our East Coast clients, but for some reason WordPress shelved it. I went in and manually published it, so its up right now. The post is entitled IRS Filing Requirements for a Multi-Member CheckBook IRA LLC.

Hi Jordan,

I have a Checkbook IRA LLC and just completed a real estate transaction where the LLC was the owner/seller of the property. The closing agent now wants to send a 1099 to the IRS and to me, and have asked me what TIN to use on the 1099. Since the LLC is a single member disregarded entity and has no TIN, what number do they use on the 1099?

Hi Jeff,

When the LLC was set up, a EIN or Federal Tax ID number should have been applied for and issued to the company. If the LLC does have a EIN, you should fill out a W9, and if its done correctly, no 1099 should be issued. Its hard to get more specific than that because we didn’t set you up.

I’m surprised whoever set you up didn’t secure an EIN for the company.

I have an IRA owned LLC. The LLC owns property which it rents and owns some financial notes, both of which generate payments to the LLC. I wonder if the LLC owes taxes in Maryland, or does the income pass through to the IRA to be taxed when I retire? Thanks

Hi Jeff,

Is the property owned by the LLC in Maryland?

Hi Jordan, I am reading all this good information but not quite understanding the 990T requirement. I have not heard of this until today. Yikes. I have a checkbook roth Ira LLC and currently am investing in private money lending for real estate based loans. How do i determine if I should have filed and paid tax via 990T? My CPA did not alert me but I know she is not very familiar with the Checkbook IRAs.

Hi Gail,

The 990T tax return is only required when taxable income is generated, and tax is due. With the investments you’re doing, you don’t have to worry about generating taxable income, and so won’t need to file a 990T. If you have any other question, let me know.

thanks,

Jordan

Your site did not pop up in the hundreds of times I have searched on variations of IRA LLC. I am grateful that I finally found it. I’m in the process of paying $25 to redo my Florida LLC to make my IRA the sole member and to redo the “manager” designation. I’m in the process of writing an operating agreement … but will call you to discuss who should write it. Thanks so much.

Thank you for the compliment, Louise. Our goal is to add value to the IRA LLC community. There are a lot of people visting this site who aren’t clients, but don’t seem to have any place to go with their questions because the company that set them up won’t answer the phone or won’t get back to them. I’m glad we can provide a place where those people can get answers and use the IRA LLC correctly.

thanks again,

Jordan

Hi Jordan. With a single member IRA LLC do I have to file form 8832? Thanks so much for your fine service.

Hi HHD,

Thanks for the compliment; I’m glad our site is helpful to people like you.

The IRS automatically disregards a single-member LLC for filing purposes. The only time the LLC would need to file form 8832 is if the LLC didn’t want to retain a disregarded status, and instead wanted to be treated as a C-Corp for tax purposes. Hope this helps!

Jordan

(I hope this doesn’t post multiple times. I am having trouble with the website for some reason. Not getting positive confirmation of post and also getting some error messages from browser, Google Chrome.)

Thanks, Jordan, but I need some further clarification. There are 2 IRA’s which own the LLC. In the operating agreement, my lawyer elected to be taxed as a partnership, but then went on to write that form 8832 will be required. Also, in obtaining the EIN, he specified partnership, and the letter I received from IRS says that form 1065 will be required. Is that all correct? I need to get a proper understanding of all this. Again, thanks very much for being here. (p.s. – I cannot go back and ask the lawyer because we had a falling out over some obviously wrong things that he did in the process, so he is no longer my lawyer.)

Hi again,

The IRS automatically classifies a multiple member LLC as a partnership. The purpose of form 8832 is to change the default tax classification the LLC originally receives. So for example, if a two member LLC secures an EIN, the Service automatically treats the LLC as a partnership. Form 8832 would need to be filed if you wanted the LLC to be taxed as a C-Corp.

To the point: if the LLC has already been classified as a partnership when the EIN was secured, you would not need to submit form 8832.

(again, still having browser troubles!)

Update. I have been reading forms 8832 and 1065 instructions and here are my (layman’s) conclusions. Two IRA’s in

LLC is a partnership by default, and disregarded entity is not an option, so 8832 is not required as it is not going

to be a corporation either. Even though a partnership, 1065 is also not required because the entity will have no

taxable income from the IRA’s, and therefore no deductions are possible either. But this raises another question:

can the IRA owners deduct LLC and IRA fees and other expenses paid “out-of-pocket” on their personal tax returns?

After all, the LLC expenses are incurred for the benefit of the IRA’s. Thanks in advance.

Since the LLC has multiple members, and has been classified as a partnership by the IRS, the LLC must file the 1065 return. An entity that is treated as a partnership must file the 1065 return, irregardless of who the owners are. In this case, the LLC is not exempted from filing the return because two IRAs own it. You’re right that the income back to the IRAs would not be taxable, but the 1065 return still needs to be filed.

As to the question of fees: as a general rule (with a few exceptions), any fees incurred during a transaction or investment made by the LLC need to be paid by the LLC. So, if the LLC purchases a property, any closing costs, property taxes, realtor expenses, etc… would have to be paid by the LLC. Under certain circumstances, the Manager of the LLC may take on expenses and be reimbursed by the LLC, but that depends entirely on how the legal documents of the entity have been drafted. IRA fees can generally be paid by the IRA owner; not all Custodians will let you do it, but a lot of Custodians now will let you reimburse the IRA for fees incurred during the year/quarter.

To put it more succinctly, IRA fees can generally be reimbursed by the IRA owner (although I don’t believe you can claim reimbursements as a deduction on your personal tax return.), but fees incurred by the LLC must be paid by the LLC, and not you personally.

Copied from form 1065 instructions:

“Who Must File

Domestic Partnerships

Except as provided below, every domestic

partnership must file Form 1065, unless it

neither receives income nor incurs any

expenditures treated as deductions or

credits for federal income tax purposes.

Entities formed as LLCs that are

classified as partnerships for federal income

tax purposes have the same filing

requirements as domestic partnerships.”

It seems to me that the 2 IRA LLC will not receive income, nor have deductions for income tax purposes. Therefore, the form should not be required. But, I guess the only harm in filing it would be the possibly unnecessary time and cost of doing so. Thanks.

I have established an IRA, LLC in KY … applied for and received an EIN from the IRS … went to my bank to open a self directed account but they ran me thru their investment counselor to act as custodian and they only offer publicly traded securities. I want to buy a private share in an oil well in the IRA which the bank cannot/won’t do (their self imposed limitations). I had them sell the public security the IRA was invested in and return the cash to the account to be able to buy the share but now need to know what mechanism to use to make this happen. I guess I need a new Custodian? This is time sensitive (by June 28). Can I open an account with IRA Services as Custodian, do a “rollover” to them from US Bank and instruct them to mail a check to secure the share?

Further to my former … can I open an account with IRA Services (for example) and appoint them custodian without transferring assets … and simultaneously, open a bank account in the name of the IRA, LLC using the EIN I received from the IRS … then cut the check to purchase the share myself … and then report ownership of the share within the IRA when prompted by IRA Services?

Hi Jon,

I think it best that you call me directly. You can call us at 1-800-482-2760. The oil well investment you have in mind is perfectly allowable for qualified funds, but you need to make sure everything is set up correctly before you make the investment.

I realize this is a time-sensitive issue, but it is far better to pass on this investment, than to go forward in a slipshod manner, as doing so can risk the tax deferred status of your IRA. Give me a call, and I’ll see what we can do for you.

Hi Jordan. Must the fees to setup the LLC be paid by the IRA’s? If there are 2 IRA’s, must the setup fees be split in direct proportion to each IRA’s capital contribution to the partnership LLC? Thanks.

HHD,

It is generally advisable to pay the setup fees from the IRA, and also advisable to split the fee between each IRA. Making sure the setup fee is split up in proportion to the capital contribution break up of the LLC is probably splitting hairs, but it can be done as well.

I was researching and see your Q/A. I’ve already paid for the IRA LLC setup but used our other LLC to pay for it. Can’t figure out how one would pay for an LLC setup with an LLC that isn’t set up yet! Question: is this going to be an IRS problem because the IRA did not fund the new LLC?

Great stuff from you – thanks a bunch!

Hi Diane,

Without knowing more of the details, I’d have to recommend you talk to the company that set you up about payment. Most people pay their setup fee from their IRA, after the structure is in place. Payment can be made with personal funds, under certain circumstances, but it depends on the situation.

Sorry I can’t be more help.

Hi Jordan. I have an IRA LLC. I want to create a foreign LLC and fund it with the IRA LLC as one member and personal funds as another member. What is your opinion of this plan?

Thanks very much in advance.

HHD

Hi Jordan. I’m adding on to my previous question. The personal ownership percent of the foreign LLC would be about 30% with 70% owned by the IRA LLC. From what I have read, this should be OK since the related party ownership of the company is less than 50%. Do I have this right?

On a related subject, I need some clarification. My IRA LLC has 2 IRA owners, me and my wife. My extensive research and opinions sought led me to conclude that this was perfectly OK. But now I am wondering why are these 2 IRAs not related parties? Thanks.

HHD,

I would not suggest setting up an entity that is owned partly by you and partly by the IRA LLC. I suppose it can be done theoretically, but it would be rife with difficulties that would outweigh any benefits of being able to combine your funds into one structure.

A husband’s IRA and a wife’s IRA are considered related parties in the context of 26 USC 4975. Neither IRA can deal with the other. That’s not to say an LLC can’t be set up with the two IRAs as co-owners, it just means there are some things to keep in mind. The grey area is the question of whether or not additional funds can be brought into the LLC from each IRA, subsequent to the initial funding. I don’t have an answer for that, other than to say a conservative position is to refrain from any additional funding.

Hi Jordon,

My husband and I funded our checkbook LLC in 2010 for the purpose of buying/selling real estate with our IRA monies. The tax attorney that set up the LLC and simultaneous funding for both of us seemed to be very informed and thorough. However, our CPA does not appear to have as much knowledge about SDIRAs as our tax attorney did. YOUR SITE AND KNOWLEDGE IS THE BEST ON THE WEB! I’ve been doing alot of self education online for the past couple of years and finding your site today was like getting a wonderful early Christmas gift! Thank you for all your posts!

Now, for my concerns…. our CPA advised us that we only had to pay the annual CA state fees of $800 for the LLC and said no fed return was required because no taxes are paid. It was just a couple months ago that I differed with him when I discovered that forms 1065 & K-1s were required because it’s a “multi-member LLC” (husband & wife). When he discovered that I was correct, he proceeded with filing the appropriate federal returns (just completed). He said he didn’t realize the LLC was multi-member because he didn’t know that husband/wife could invest IRA monies into one LLC (uggg). He said there are no penalties for late filing 2010, 2011 & 2012. Is this correct?? I know that that there is no tax due on the profits of sales since none of the properties were ever financed, but aren’t there penalties for not filing on time? I’d really like someone as knowledgeable as you to verify that. All 3 yrs were just sent in this week, and I guess I’m a little nervous about possible penalties or other ramifications for filing 3 yrs so late!

He filed the 1065s in the name of the LLC and a K-1 for each of us. Part II-F on the K-1 shows the IRA custodian’s name and then “FOR” with our name & address under the custodian name. He has our personal SS# for Section II-E. Is this the proper way to complete the K-1, (so the IRS knows there is no tax due)? The disregarded entity box is checked “no”. I assume this is because it’s a multi-member LLC. I’m pretty sure he did this right, but based on the lack of knowledge he displayed about husband/wife multi member rules, I’m not real confident, so I’ve been looking at the returns with a fine tooth comb now. He’s always seemed to be a competent CPA, but apparently not very well versed with SDIRA rules. It seems that many CPAs are not really up to speed with IRS rules & tax filing requirements in this arena. Again, I must say how refreshing it is to find you and all your “in depth” posts. Thank you!

Hi DJ,

Thank you for your kind comments. I’m always glad to hear our site is helpful to both our clients, and to others who use the Check Book IRA structure.

While we don’t offer tax advice, I don’t believe there would be any penalties for the late filing; especially considering no tax was due in the first place.

In regards to the K-1, it can be a bit confusing, but thankfully the Service has added a box on the new K-1 which allows you to notify the IRS that the partner is an IRA. The K-1 instructions state

, and the instructions for form 1065 state

So, the IRS wants the name of the IRA (IRA Services Trust Co. or whatever Custodian you use cfbo Jane Doe IRA), and the Tax ID of the Custodian, not the SSN of the IRA owner. The IRS is contradictory on this point at times, as on the SS4 form they require the IRA owner to use his/her SSN as the identifying number for an IRA, so they’re not exactly consistent. In any event, for the 1065 and the K-1, the instructions say they require the TIN of the Custodian to the IRA. Since the LLC has more than one member, the IRS will automatically classify it as a partnership for tax purposes. The LLC would be considered a disregarded entity only if it were a single-member LLC.

The question of filing requirements for IRA related investments and IRA owned entities can be confusing, mainly because so few people use IRAs in this way, in proportion to all other retirement accounts held in publicly trade securities, that the IRS has not put much effort into bringing clarity to some of these issues. To illustrate the point, my guess is that less than 1/30th of 1% of all retirement accounts in the nation utilize structures like the Check Book IRA. There are even some very competent CPAs that would argue a multi-member IRA LLC does not even need to file a 1065 so long as the LLC did not incur any UBIT or UDFI taxable income, because the 1065 instructions indicate that a partnership that receives no income is not required to file a return, and goes on to state that a 501(c) should only file a return if it has taxable income. The IRS will no doubt attempt to provide some clarity on these issues in the future, if nothing else, as a response to more and more people using them. Its definitely a good thing to see the K-1 utilize a box identifying the partner as an IRA, and also good to see some instructions regarding how to list the IRA on the 1065.

If you have any other questions, let me know. As I said before, we don’t give tax advice, and everything I’ve just talked comes directly from the K-1 and 1065 instructions, but if something else pops up, I’ll be glad to help if I can.

A couple questions come to mind as I read your response to DJ’s question:

(1) I have to file an 8832 for a client of mine to elect for their foreign LLC to be treated as a disregarded entity. The self-directed IRA is the owner of the foreign LLC so I am uncertain as to who should be listed as the owner on Line 4 of the Form 8832. I was inclined to list the client and his SSN, but you say for the 1065 and K-1 the custodian’s name and EIN should be listed as the owner. Which should I use for the 8832, or would both be acceptable?

(2) Also, my client’s Foreign LLC has both the husband and wife named as members, so he entered “2” for the number of LLC members on SS-4. For domestic LLC’s, if the 2 members are husband and wife, then it’s still considered a single member LLC by default. The SS-4 (stating 2 members) has already been submitted for the EIN #, but now that I’m doing the 8832, I’m wondering if the IRS will a reject the election to be treated as a disregarded entity if they see that the LLC reported two members on the SS-4. Should I call the IRS and have the SS-4 amended to read one member since the only two members are husband and wife?

Thank you so much in advance for your help. I’ve been spinning my wheels doing research on all of this and your articles and forums have been invaluable to me. 🙂

It was good talking with you today, Dianna. I hope all your questions have been answered.

For everyone else: I hesitate to try to answer these questions in the comment section, simply because in this situation it is best to talk with someone about the specific situation, so that all of the ins and outs of the situation can be taken into account.

If any of you have questions of this nature, it is best to call us. We’ll either answer your questions, or put you in touch with a professional who can help you.

Hello, I’m looking for some guidance or to touch base with someone who has experience with IRS “Response form for Form 1065.”

Background, I have a a single-member IRA LLC for purchasing real estate and property tax liens, and everything is cash-cash-cash, no loans, nothing funny, just what I can afford out of my checkbook LLC.

Yesterday I received a form from the IRS asking why I had not filed an IRS Form 1065 for tax year 2012. Its been suggested I fill out the form with:

“this LLC is not a partnership, but rather is a single member disregarded entity for which an IRA is the sole owner. As such, no tax filing is required. The reporting for the IRA was accomplished with the 5498 filing of the IRA custodian.”

And while this answer/information makes perfect sense to me, wanted to know if anyone on this blog had run into something similar. And if yes, how did you answer the IRS? Is this a common occurrence? (hopefully not)

Note, the information and presentation of information on this posting has been a benefit, as my tax preparer nor her CPA had a clue how to provide guidance. CPA, “you have a what that owns what? I’ve never heard of that before.” Me, “I humbly suggest you do some research as this may be the first time you hear about this, but trust me its not going to be the last time.”

Ok thanks in advance, Bob

Hi Bob,

Thank you for the compliment. I’m always glad to hear that our articles are helpful to our clients, and others.

Your situation is easily remedied. The Form 1065 return is required of partnerships, and if the Service is asking why it has not been filed, it means that according to their records, the LLC is a partnership. Whoever applied for the Tax ID number must have mistakenly listed the LLC as having multiple members, and the IRS must have automatically classified the company as a partnership.

Although we don’t give tax or legal advice, the information for the LLC must be changed with the IRS to reflect that the LLC has only one member, and is therefore, and has been since it’s inception, a single-member disregarded entity. What you put in your comment “this LLC is not a partnership, but rather is a single member disregarded entity for which an IRA is the sole owner. As such, no tax filing is required. The reporting for the IRA was accomplished with the 5498 filing of the IRA custodian” is very good. The only thing I would add is to point out that the LLC did not begin as a partnership and then become a single-member LLC, but was a single-member entity from it’s formation, and that the SS4 or online EIN application was completed incorrectly.

The IRS requires that any changes to an entity’s EIN account, be made in writing. Once the letter is drafted, it may be mailed to the EIN Operation section of the IRS’s Cincinnati, OH office.

You should receive a reply from the Service within a couple weeks, informing you that the LLC’s information has been updated.

I hope this has been of help. Good luck investing!

Jordan,

Thank you for all the great info. When filing a 990t, do you file in the name of the IRA account held with IRA services and use the associated EIN, or do you file in the name of the IRA LLC and use the LLCs EIN?

-Mo

Hi Mo,

The 990T return is a trust return, so it is made in the name of the IRA. You’d need to talk with your Custodian, but generally, if the IRA is filing a tax return, it is required to secure a Tax ID for the IRA itself.

Thank you, and I will call my custodian for more info.

Another question, is it ok to make payment to the IRS from the IRA LLC checking account, instead of the IRA account with the custodian?

-Mo

Mo,

The tax is actually incurred by the IRA, so any payment of the tax needs to come from the IRA itself, and not from the LLC.

Excellent info!

My self directed checkbook ira LLC is opening a mutual fund account to park idle cash between hard money real estate loans. Do I simply use the LLC name and EIN to open the account with me as the authorized agent? Do I just check the box for LLC and the “not subject to back up withholding” box?

Thanks

Hi Richard,

Thanks for the compliment.

Whatever accounts you open for the LLC, need to be in the LLC’s name. The brokerage house will probably require the Operating Agreement, EIN, and filed paperwork showing the LLC legally exists. As to the “not subject to back up withholding”, that depends on how the LLC was filed and what information was entered on the SS4 when you applied for the EIN. Having said that, the LLC probably is not subject to backup withholding. If you’re filling out the W9 for the new account, make sure you talk to a CPA first, because there’s a certain way the W9 has to be filled out for a single-member IRA LLC.

Great article about filing requirements, Jordan. Thanks for writing it. I have IRA services as my custodian. Are we supposed to get a copy of the form 5498 when they file it with the IRS? Or can we just assume that they’ve completed it every year?

That’s a good question, John, and quite frankly I don’t know the answer to it. Being an informational return, it probably should be sent to you as the IRA owner, to double-check that the numbers match with your books, in regards to contributions, distributions, rollovers, etc…

I would suggest you call IRA Services directly to see what their policy is on that.

I want to find out if I can set up a Multiple Self Directed IRA for the purposes of purchasing my existing home? I currently rent out 3 of the 5 bedrooms in the home and report the income on my annual taxes. I was curious however if there is an IRS limitation on purchasing my own property and considering it as an investment for purposes of being a rental. It would reduce my existing liability, it would be an investment in that it returns an annual income, but I wonder if this is not allowed as it is ultimately also the place that I live as well. I know folks purchase multi-family’s and live in the other half in duplexes. Just wanted to know if this was an option one could consider. Also, can you point me more specifically to the IRS regulations around the Self Directed IRA? My wife is not convinced that any of this is above board. It sounds reasonable and accurate to me but would love to find more specifics from the IRS as well. Also, is the income that we put back to the IRA from a Rental something you would report separately and be taxed on? Or is this deferred at this point in time? Appreciate the article and look forward to your guidance.

Hi Eric,

You would not be able to do what you have in mind. Any deal or transaction between the IRA and any disqualified person is prohibited. The fact that you rent out the other 3 rooms, is not a factor. You could even move out entirely, and rent the house to someone else, but you still would not be able to sell it to your IRA. The sale would be a transaction between you and the IRA, and that is specifically what is prohibited. Neither could your IRA assume the mortgage on your house, as that would constitute a transaction as well.

As to your second question regarding how rental income is treated, first off you’d have to make sure the house the IRA buys is not your own, or any other other disqualified person’s. With that out of the way, if the IRA were to buy a house from an unrelated third party, the rents would go back to the IRA, and would not be taxed. If you were using an IRA LLC, the rental profits would go back to the LLC, and would also not be taxed.

Your wife’s questions about what the IRS has to say about self-directed IRAs, is hard to answer because of the way IRA law works. The term “self-directed IRA” is a bit of a misnomer. An IRA is an IRA is an IRA. Were you to have two IRAs, one at Fidelity, and another with a self-directed Custodian, each IRA is the same. Its not as if the self-directed IRA is an entirely different structure, or a different kind of IRA that has it’s own rules or something like that. IRA law, which applies to any IRA that is opened under any circumstances at any Custodian, is not positive in the sense that it says “you can do this, that, and the other thing with this IRA”, it is actually negative in the sense that it says “you can do anything you want with your account, except these specifically listed things, or except for this particular restriction”.

With that in mind, there are only two sets of restrictions on IRAs. The first has to do with specific investments that are prohibited to an IRA. IRAs are specifically prohibited from purchasing life insurance contracts [26 USC 408(a)3] and also from buying anything that can be considered a collectible [26 USC 408(m)]. The second has to do with persons and entities that cannot deal with or benefit from the IRA. Those rules are set out in 26 USC 4975.

Those are the only restrictions that have ever been placed on IRAs, so investing in real estate, precious metals, or offshore is nothing new. More to the point, if you visit the IRA FAQs page on the IRS.gov website, you’ll see what I mean. On that page, the Service is quoted as saying:

When you look at the code, and at different court cases that have to do with investing with IRAs, you’ll see that the concern of the IRS is always, always, always, someone using their IRA as a tax shelter; trying to hide personal income in the IRA so that it escapes taxation, or pulling funds out of the IRA through some back-door deal without paying taxes, or cooking up some scenario where they benefit from the funds, while they’re still in the IRA.

The government doesn’t mind a person growing his retirement account, because they’re going to get a piece of it anyway, so the idea that non-traditional type investments are outside the norm for IRAs is just not supported by the facts. IRAs have always been able to buy real estate, and any number of other non-traditional investments.

Thanks for the questions, and let us know if you have any more.

How do you fill out a W-9 for a self-directed single owner IRA LLC.

Do you check the LLC box and put a D as the type for disregarded entity, or do you check the Individual/Sole proprietor box?

I have an EIN for the IRA, which is different from the EIN of the LLC. Should I use the EIN of the IRA, or my SSN for the TIN? In the name filed I assume I put my name, and the name of the LLC in the Business Name.

Thank you in advance for any guidance.

John,

It was nice talking with you today. I’m glad we were able to get you lined out with the W9. The firm that set you up should have known how to complete the W9, but I know you said you had trouble getting in touch with them.

We’re always here to help our clients (and even non-clients), so if anyone you know plans on setting up a Check Book IRA, we’ll be more than happy to help them.

Thanks for your valuable advice, when do you find time to sleep?

I just opened a Checkbook IRA to purchase a vacation rental condo in Florida. Does the LLC have to pay the monthly sales tax for the rental income?

Thanks

Ernie

Ernie,

I don’t know if I can answer that question. Even though the IRA owned LLC doesn’t pay any income tax, it still might trigger more localized taxes such as the sales tax for rental income, or a State mandated franchise tax (which isn’t an issue in Florida). I’d suggest you call a local CPA and see what they have to say about it.

Good luck!

I am working on applying for my LLC EIN, however I want to ensure I am completing the SS-4 correctly. The way this is structured is that my custodian is the 100% owner of my LLC (resulting in a SMLLC), of which I am the manager. Am I correct to list myself on line 3 as the person in “care of “? Second question, I assume I list the custodian on line 7a along with their EIN on 7b? If so, do I also put “FBO my name LLC” at the end? I tried that and my EIN application got rejected stating the name and EIN number do not match our records? Thank you for any insight you have.

There are a few different ways to complete the SS4 depending on your situation, and the Custodian you’re using. I would suggest contacting the company that set you up with the IRA LLC. They should know how the form needs to be completed, based on how your structure has been set up.

This website is the single best source of information I have come across for the SDIRA. Thank you.

I want to open an IRA/LLC that I believe will incur UBIT (buying and selling cattle). I’ve seen references to creating a C Corp to reduce taxes but no explanations. Is the C Corp a separate entity in the mix or does using form 8832 to change the LLC’s tax status create the C Corp?

Thanks for the compliment, Michael.

Whether buying cattle would trigger UBIT depends on a few factors, so before settling on a C-Corp I would suggest you call our office so we can talk about what you have in mind.

If you were to decide to use a C-Corp, there are a couple of ways you could do it. You could create a C-Corp, or you could create an LLC that elects to be treated as a C-Corp for tax purposes, which would require the 8832 as you mentioned.

We can talk about it at greater length on the phone, but essentially, if an IRA is going to trigger UBIT, it is sometimes advantageous to do the investments through a C-Corp so that the C-Corp takes the tax burden, and not the IRA. IRAs are trusts, so if they trigger UBIT, they’re taxed at the trust rate, which is absurdly high once you get above about $15k in income. The strategy is to have the C-Corp handle those investments, pay corporate tax, and then pass dividends back to the IRA tax-free/deferred. The corporate tax will almost certainly be lower than what the trust rate tax would be, so that’s the strategy in a nutshell.

Feel free to call us at 1-800-482-2760, if you’d like to talk more about it, and thanks for your question.

Jordan,

You provide some really valuable info!!!

For the K-1, my investment partner is asking whether my self-directed IRA LLC is a limited liability company corporation or limited liability company partnership. I am the only member who controls the LLC

On section G it asks whether I am a limited partner or general partner.

Also on I1, what type of partner it is ? Is it IRA ?

Appreciate your help

Best

Balaji

Hi Balaji,

We don’t give tax advice here, but I’m happy to put you in touch with an excellent CPA we work with.

I own a CheckBook IRA LLC and your answer regarding Federal tax filing requirements was extremely clear and helpful.

Mine is a State of California LLC and the state’s phone assistance line is telling me I have to file CA form 568 and Pay an $800 annual fee which I do not like but understand. They are also telling me I have to report my income and pay additional tax on that income which does not seem right as it should be tax exempt. I do have to pay tax, this would be paramount to double taxation since I would have to pay state tax again when I finally get distributions and report them for federal tax purposes.

Thanks in advance for your help.

Hernando

Hernando,

I feel your pain, believe me. California is by far the most expensive State in which to maintain an entity. Unfortunately, the $800 franchise tax fee is something that is required, and infuriatingly despite the fact that the owner of the LLC is a tax-exempt trust, the State essentially says “We don’t care, we still want our $800”.

It sounds like the $800 fee came as a surprise to you. Whoever set you up with your IRA LLC should have made those yearly expenses clear before setting up the structure.

Almost all States charge some sort of yearly fee to LLCs. Some States call it an annual report fee, or a annual renewal fee. Other States such as California, Texas, and Tennessee have what’s called a franchise tax system. Its not an income tax, but a tricky way the State can charge the LLC more for the right to exist. Basically, the franchise tax is a graduated tax, and the LLC must report it’s income for the year to figure out which tax bracket it is in. The brackets are not a percentage of the income, but set dollar amounts. So in California, $800 is the lowest bracket. Once the LLC gets up over $250,000 in income (I think), the fee goes up to something like $1,200.

Again, the franchise tax is not an income tax, but more of a compliance tax. The tax has to be paid for the LLC to continue to have the right to exist and do business in California. You can probably see now why business have been running away from California for the last number of years.

The bottom line is, the LLC will need to file that 568 form and pay the $800 franchise tax fee. Pretty much any CPA can do the return for you, as all entities in California are subject to the franchise tax. I wish I had better news for you.

As a final note, and for all others reading this comment, one strategy that we use for our California clients is we set them up with a Solo 401(k) instead of a Check Book IRA. The Solo 401(k) has certain requirements that have to met in order to to qualify for the plan, but the Solo 401(k) doesn’t require an LLC, and so you don’t have to worry about the franchise tax fee. We set up Solo 401(k)s, so if its something that interests you, give me a call and we can go over your options.

Hi Jordan. Great website! Apologies if these topics have already been covered but I keep finding conflicting answers to some very key questions:

1. After the LLC is initially formed and capitalized are subsequent contributions allowed? There are some out there who say they are and others who say it would be a prohibited transaction. If you can’t make any additional contributions without violating the rules then it seems it would not make any sense to have this type of structure unless you have a large sum of money to capitalize it with. I am 35 years old with 25 years until retirement. What I would like to be able to do is make a modest initial contribution and then make additional contributions each year going forward. Do you have an official viewpoint on this?

2. In the case of an LLC that is a partnership where for example my Roth IRA owns 67% and my HSA owns 33%, would one member be able to take a distribution (and hence the percentage of ownership of each would be adjusted accordingly) or would both have to take a distribution pro rata to stay in compliance with the rules?

Thanks for the help,

Phil S.

Hi Phil,

Good questions.

If the LLC is a single-member LLC, there are no problems with the IRA adding funds to the LLC. The IRS dealt with this issue in IRS Notice 2012-52, when they identified a single-member LLC that is owned by a tax exempt entity, to be an extension of the tax exempt entity. That means if the IRA moves more money to the LLC, it is not a transaction that could be prohibited, as the LLC is an extension of the IRA. There is a lot of confusion on this point.

It should be noted though, that as soon as the LLC becomes something other than a single-member LLC, there can be issues. Leading into your next question, if the LLC is owned by two IRAs, the LLC is no longer a single-member, and no longer disregarded. There would seem to be some problems adding funds in that scenario from either IRA.