IRA LLC Asset Protection

The Problem

“I earned it, YOU can’t have it… it’s MINE”

The only thing worse than not making any return on your IRA is losing it through a lawsuit. A few are in high risk professions, but is anyone really safe from lawsuits? You need added Asset Protection.

How about being sued because your coffee is hot? Consider the now famous McDonald’s lawsuit concerning a lady spilling hot coffee on her lap after leaving the drive through. You’d think, since she was in her 60’s, that she’d know by now that coffee is generally hot. However, the jury found McDonald’s not only guilty of serving hot coffee but ruled that she had suffered enough to be awarded millions!

My wife’s hair dryer has a tag on it warning “DO NOT USE IN SHOWER”. There’s no common sense. Frivolous lawsuits are rampant.

“What?? A judge could decide how much I retire on?”

Yep, The US Supreme Court ruled that a court could decide how much of your IRA you get to keep if you lose a lawsuit allowing your creditor access to your retirement account.

In California a state statute puts conditions on how safe your IRA is…

“An IRA is exempt only to the extent necessary to provide for the support of the judgment debtor and his dependents when the judgment debtor retires, taking into account all resources that are likely to be available at the time of retirement.“

The Solution

Our CheckBook IRA is a tool that could keep a judge from deciding just how much of your own retirement is “necessary” for your support. You will sleep better at night knowing the IRA LLC provides powerful asset protection.

HOW AND WHY IT WORKS

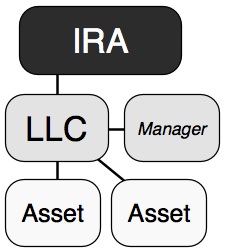

The IRA-LLC. This is the key that makes the CheckBook IRA so powerful. First we move your IRA to a Self-Directed Custodian, one with no investments to sell you. We help the IRA form and own a special customized LLC (limited liability company). YOU are named as the manager and have the sole signature authority. The LLC is a legal entity that has powers and protections that are not possessed by any individual or by any regular IRA.

It is the combination of the self-directed IRA custodian, our special LLC and all the proper paperwork that yields such beneficial results. You are the manager.

It is the combination of the self-directed IRA custodian, our special LLC and all the proper paperwork that yields such beneficial results. You are the manager.

It is started, created and owned entirely by your IRA. An LLC that is designed specifically for an IRA, that respects IRS and Department of Labor codes governing IRAs. The legality of an IRA owning an LLC was affirmed in the case Swanson v. The Commissioner in 1996. In fact the case for the IRS was deemed so weak that the Tax Court forced the IRS to pay the $50,000 court costs incurred by the IRA owners.

Please note that an IRA owned LLC is different than a regular LLC. One of the lessons learned from the Swanson case was the LLC must formed in a particular way and contain very specific language that meets all IRA codes and requirements, and that satisfies the Department of Labor (DOL). Once formed you as manager must see to it that all rules are strictly followed.

If the LLC is improperly drafted, the entire LLC IRA may be disqualified and taxes and penalties would be assessed. Needless to say, you do not want this to happen! Not to worry, we will handle this transaction from start to finish to make sure it is done according to all the rules and guidelines.

“WHY DO I NEED TO USE AN LLC?”

An LLC (Limited Liability Company) is a business entity that is a cross between a corporation and a partnership and is the PERFECT investment vehicle for your IRA! It gives the liability protection of a corporation, that is to say, even if you own all of the LLC, you nor the IRA can be liable for the it’s debts. At the same time it can be taxed as a partnership. This is favorable as the LLC itself will not pay any taxes, rather, it will be the owner of the LLC is liable. But in your case the owner is your IRA. The tax bill will be determined as if the IRA earned the money profits – NOT the LLC.

In short, an LLC is a separate legal entity whose tax liability passes through to the owner of the LLC even though the funds might, at the manager’s discretion, remain in the LLC. As a result of this strategy no taxes will be owed on the passive profits generated in the LLC, using your Check Book IRA. The profits stay in the LLC readily available for reinvestment and the tax isn’t due until you take a distribution from the IRA.